#48: Sailing into the Uncharted: Compounders Prediction on 2023

1.10.2023

To stay in touch, you can find us here: Gabrielle's Twitter and Shan’s Twitter

HNY friends, hope you all had a great holiday slow-down to relax and recharge. We are excited for the year ahead and can’t wait to share with you our predictions for the year. To be frank - these predictions are a mix of pessimistic and optimistic views, and that’s our honest thoughts for what 2023 may shape into. Now, let’s dive in:

Gabrielle’s prediction on Macro & Public Market

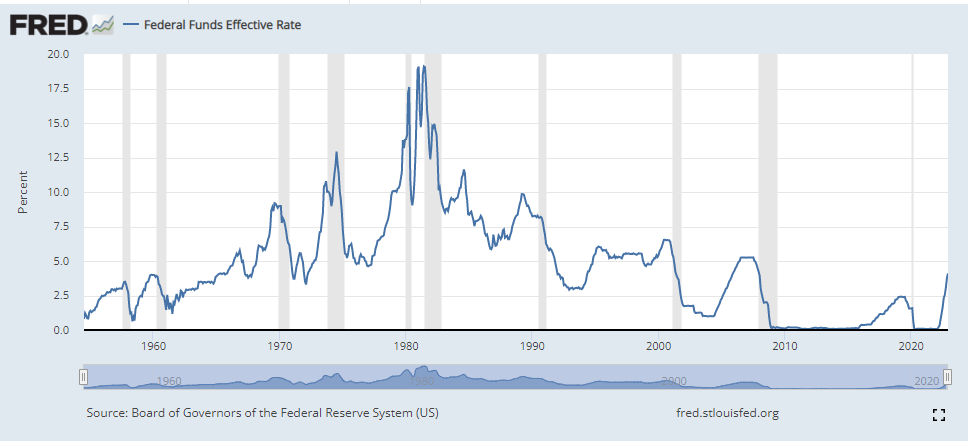

1. End of a 40-Year Cycle: Re-Calibration in Progress

What happened in the past 40 years? The last 40 years marked a consistent downward trend of interest rates, which painted the best possible picture for the US economy: low inflation, low-interest rate, and high growth. Some historians argued that it all started with Arab-Israeli War in 1973, where OPEC imposed an embargo against the US in retaliation for supplying the Israeli troop, which led to a rising oil cost driven by supply-side constraints. In comparison, economists blamed the abuse of Keynesian economics, which led to the wage-inflation spiral and ultimately trigged inflation. Either way, the US economy ran into a long-lasting battle with inflation, where CPI reached 14% in 1980. This was when Volcker stepped in, brought the fed fund rate up to 20%, and got inflation back to control to 3% in 1983.

Since then, the interest rate has been declining decisively for four decades. Why do we say the old cycle is ending now? Because 1) the magnitude of the rates hike exceeded the previous eight hikes and broke the pattern of the past monetary policy 2) 40 years of economic expansion comes at a cost — national debt. US Debt to GDP now accounts for 123%, which is unlikely to sustain. A higher interest rate buys the government more time to fight for a debt ceiling budget 3) The most significant deflationary factor has been deglobalization. With the supply chain reshoring, US/ China power struggle, and the Russian / Ukraine war, It is inevitable that the world political system is becoming more polarized, which means future trade will be conducted at a higher cost.

We are entering a new phase of the interest rate environment. The magnitude of change can be so enormous that Howard Marks calls it a “Sea change” in his recent memo. We highly recommend our readers to take a read as it is imperative to know as we enter the 3rd largest cycle change over the past 50 years, along with the Volker moment in 1980 and the invention of the High yield bond in the mid-1970s.

The game has changed for investors. For 40 years, almost all investors benefited from a high-growth, low-interest rate environment. PE and VC investors benefited from excessive liquidity and high leverage, while tech investors enjoyed a 10-year bull run in the public market. Needless to say, interest rates played a significant role, if not the biggest role in historical returns. Going into the future, we expect to see a re-calibrate of the return generation algorithm. Private investors won’t be chasing after growth at all costs. PE return is likely to be compressed, while high-yield bonds could outperform. Public investors will return to stock picking 101, spending more time finding real compounders with pricing power that can survive a high-interest environment. This means no more “Lazy longs”; only alpha-generators can survive. Companies that can’t figure out growth in a high interest-rate environment will quickly go bankrupt. As cruel as it sounds, high-interest rates often demand higher returns, and we see more opportunities in technology and high growth over value.

2. Fed Action: CPI Target to be Revised to 3%. Market Bottoms in 2H. Tech / Growth Outperforms in Long-Run

For those who know me well, I don’t like to time the market. In my mind, the market bottom is something to look back on instead of forward. My strategy is to preserve the capital in the bear market, taking a calculated risk and earning an asymmetrical return when allowed to do so. That said, portfolio strategy could hinge on a few macro points worth sharing. Note that this is based on a currently available data point and is subject to change based on new inflation.

Pivot / No Pivot? The prevalent narrative believes that inflation will be tamed in 2023. It is unlikely that the Fed will lower the interest rate any time soon unless there is a severe liquidity crunch or asset price precipitate in the stock market or housing market. The Fed has a long way to go to restore its credibility, and Pivot in 2023 won’t help.

CPI Target to be revised: We think the 2% target is hard to achieve without a severe recession. Fed will likely give up some time in 2023. The reason is economic activities have slowed down significantly: Service PMI came in at 49.6 vs. 55 expected, suggesting a contraction in economic activity. Labor market remains tight. Vacancy and unemployment are still elevated at 3 month high without a definitive trending down. My read on the recent job market data is hawkish.

3. Where to hide in the market? Rich Peoples Software and Poor People’s Consumer

While the outlook is blurry, rich people’s software and poor people’s consumers can be good places to hide. Rich people software refers to those sticky platform software with pricing power. Poor people’s consumer refers to companies that produce goods with compelling quality-to-price ratios and are still mission critical to day-to-day.

Shans’ Predictions on Thematics & Privates

4. Rise of the “Forgotten” Industries

During this winter slowdown, I took a trip to New Mexico and Texas. During this rather spontaneous trip, we serendipitously visited some exciting SMB owners in industries ranging from pistachio farms & wineries, firework factories, truck stations, art galleries (in Marfa!), and many more… Most of them, if not all, still run their day-to-day operations on Pen & Paper. On one side, we think human society is advancing fast forward with bleeding-edge technologies such as AI and Blockchain - on the other side, we believe there will be huge opportunities emerge to capture and serve these “forgotten industries” with tech-enabled toolings and platforms. These companies could exhibit themselves in the format of Vertical Marketplaces / Operating Software while deploying the power of next-gen fintech infra.

Why 2023? There already have been ample examples of vertical industry leaders, many of whom have already reached hundreds of millions in revenue - Toast, Veeva, CCC, Legalzoom. However, this category is often dismissed because of SMBs’ low willingness to pay. It’s tough to ask a firework factory owner to spend over $1k on software while they believe the pen&paper workflows are just “good enough”. What changed? We think the combination of Network Effect + Next-Gen Financial Infra Enablement tooling can bring the industry to a new high. The unbundling and re-bundling of B2B Payment, Lending, Working Capital, and, more importantly, data fragmentation + reorganization through APIs-driven infrastructure will let us think of these businesses more in Modules and Networks than pure SaaS. We are excited to see further evolution to bring these “forgotten industries” up to speed in their unique ways.

5. Blockchain Becomes “Invisible”

Sounding a bit like a broken record, we believe Blockchain, in its essence, represents two major breakthroughs: 1) decentralized data ledger and 2) a new payment rail. There are a thousand Hamlets in a thousand people’s eyes - but to us, Blockchain as a technology should be the infrastructure and rail operating in the background instead of front and center. This may get controversial: when most people walk into a coffee shop and swipe their credit card for a cup of coffee, they never really understand nor need to understand the settlement process of a credit card and the anatomy of a swipe. If successful, we think Blockchain should become the same type of “invisible” string.

How 2023? We are not here to kid anyone - we also expect a major slowdown in the sector and adoption of the technology. But we think there could emerge companies and products that don’t feel “crypto” - these companies should start, first and foremost, as a great product with real utilization value or entertainment value. 3 categories we watch are:

Truly decentralized ways of money movement

NFT tech applications outside of core PFPs.

Modularity (zkEVMs and data availability).

Many venture-backed blockchain gaming studios are slated to debut their game this or next year. For the most successful ones, games would be fun and engaging because of game mechanisms and player progression systems. Blockchain functions as a way to decentralize the storage of virtual assets and tokens, facilitate info exchanges, enable economy buildout, and many more. Consumer-facing adoption, albeit slowed, will become critical for the ultimate sizing of the industry in 2023.

6. Bear Market Breeds High-Quality Compounders

Ending 2022, we did a bit of travel back in time - looking at the ‘08-’10 financial crisis, the 2000 dot.com bubble, and the 1930 Global Recession. To many’s surprises, we found many (if not most) of the generational Consumer and Fintech companies were all born out of those troubled periods. Groupon (2008), Zynga (2007), Airbnb (2008), Venmo (2009), and Wealthfront (2008), to name a few. Coming out of the winter, we are beyond excited about putting more dollars to work because 1) the bear market instill discipline in great founders; 2) companies' models become more durable.

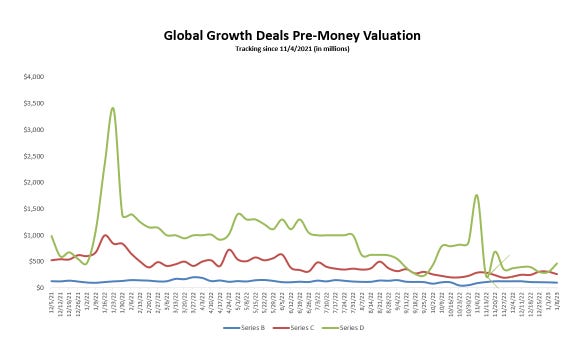

What 2023? As private market graphs exhibited below, we predict the private market to thaw slowly, but it’s hard to see it returning to the peak of the 2020-2021 period. We see Compounders companies emerging in:

Mission-critical software services (accelerated by spending cutbacks from big techs)

Value-accretive consumer platform and networks (consumers are watching their wallets, and money will only go to where the most value is manifested)

Strong intangible assets & IPs anchored healthcare/deeptech co. (human societal changes will continue to march forward)

These high-quality compounders possess characteristics of recurring revenue (anchored by behavior changes) and pricing power. Public multiples have already been reset, and we expect to see a more diverse set of deal structures coming out of Private markets - structured, secondaries, extension, and many more. The best companies will think deep and thoroughly about sustianble, efficient growth and couple that with a robust war chest. When we see birds chirping for spring, these compounders will be the next biggest winners.

Chart of the Week in the Public Market:

We started this year with a refresh of our Indices. Key changes include:

In Software: we eliminated the companies that were taken private in 2022. Names include but are not limited to: COUP, ZEN, PLAN

In Fintech: 1) InsurTech: Most of the insurtech companies have fallen below $1B market cap mark - therefore, we removed a few players that became too small to get an accurate read on EV/Rev. We kept Lemonade, Hippo, and Root. 2) Consumer Fintech: we added more international players, such as Nu Bank, MercadoLibre, and removed companies that dropped below $1B mark such as MoneyLion.

In Consumer: 1) Advertising: removed Twitter from take-private. The index is now composed of FB, GOOGL, SNAP, PINS; 2) Gaming: added PLTK and U; 3) Marketplace: remove Opendoor and Carvana from market cap requirement.

Market contracted slightly as a reversal of last week’s rebound. Strong PPI raised concern over inflation.

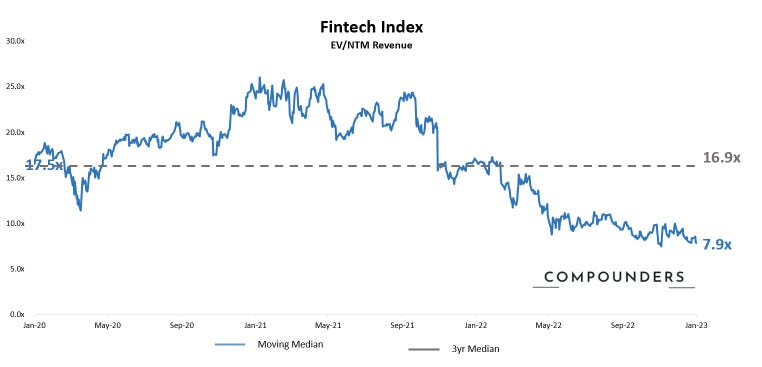

Fintech took a big leg down during the past 2 weeks - from 8.9x to 7.9x - note our main core Index remains the same with V, MA, PYPL, SQ, BILL, ADYEN, SHOP, LSPD.

With the removal of some of the smaller cap names, the Index lifted up slightly from 2.4x to 2.7x with 3-yr avg. also moved up to ~5x.

(Market data as of 1/6/2022, source: Bloomberg, CapIQ. See index composition at the bottom)

Chart of the Week in Private Market

(Deal data as of 1/9/2022, source: Pitchbook. Defined as - Series B+ global growth stage deals)

We saw a nice pickup during the last few weeks of 2022, a trailing indicator for a more active private market before the year wraps. The index slowed into winter slow-down, and we expect that low to likely track through early Jan. Also we updated the by-stage valuation chart - since tracking, Series D stage saw the substantial valuation volatility - dropping from $1.5-2B Medium to now slightly over $500M and almost overlapping with some of the Series C round valuation. Series C also dropped significantly from close to $1B to now low-to-mid hundreds.

Sources: Software Index: over 200+ public companies / Fintech Index: V, MA, PYPL, SQ, BILL, ADYEN, SHOP, LSPD / Consumer Index: ABNB, BMBL, CHWY, CVNA, DASH, DHER, DKNG, DUOL, ETSY, FB, FTCH, GDRX, GOOGL, MTCH, NFLX, OPEN, PINS, POSH, PTON, ROKU, SFIX, SNAP, SPOT, UBER, W. Please feel free to ping us for further detailed breakdown