#57: Okta Update: Re-Examing Fundamentals after the Storm

03.26.2023

To stay in touch, you can find us here: Gabrielle's Twitter and Shan’s Twitter

Okta Update: Re-Examing the Fundamentals after the Storm

Gabrielle: If you have been following my Twitter, you might remember that I had an open discussion with another Twitter friend about how we think about Okta, the largest cloud-based identity management vendor. Since then, I have done a bit of digging in on the company and want to use this week’s post to bring you all up to speed on what happened during the most recent quarters. Happy to chat over DM and share details on my work if you want to chat more. Let’s dive in:

I. Sales Challenges after Auth0 Acquisition

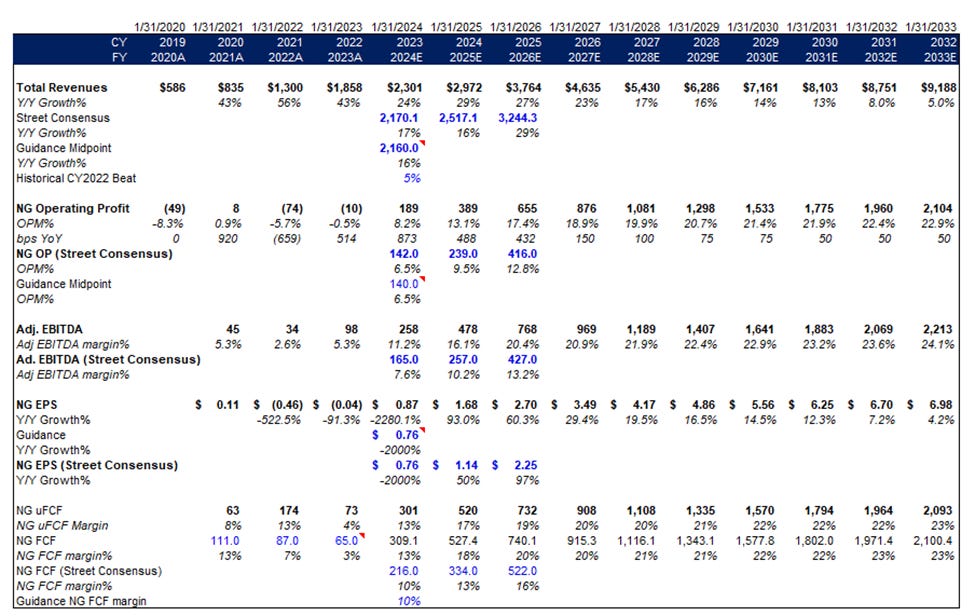

Okta is the largest cloud identity management platform that provides identity authentication and access authorization to employees and customers. It is a $13B market cap company trading at less than 6x NTM revenue. The company started with access management and single sign-on on the SMB side and has since moved up the market to address complicated enterprise use cases. Gartner ranked Okta as the Identity Management market leader for many years. The company is considered well-positioned to address the $80B workforce + customer identity TAM estimated by the management. IAM (identity access management) industry demand is driven by digitalization and the proliferation of security breaches.

Over the past year, the company has gone through a series of challenges after the $6.5B all-stock acquisition of Auth0, including management churn, elevated sales attrition, and integration challenges. When they were trying to combine two sales teams, the process was poorly managed – the product message of the two organizations was conflicting, and sales team attrition topped 20%. All these issues created pressure for new sales. Q2 FY23 was a horrible quarter when the management acknowledged those challenges. Revenue growth decelerated to 43%, falling off the 60%+ historical growth path. Delta of that growth was driven by sales attrition instead of actual operating improvement. Based on our calculator, the new ACV declined 73% as Q3 guidance suggests another 34% drop to come. Investors were spooked, and the stock price tanked 30% on the following day. Bears worry that the underperformance is driven by long-term deterioration in a competitive landscape and whitespace running out rather than short-term issues. Macro also has had a negative impact on SMB spending for the past two quarters, creating pressure on NDR. Additionally, recent management turnover like CPO, and sales leadership leaving the company did not help the stock.

II. Taking a Step Back: What’s the Long-Term Story Here

Despite the dire outlook in the near term, we think Okta’s LT growth is more durable than the market believes. As the largest standalone identity management platform across both workforce and customers, the market is theirs to lose. While there has been an everlasting debate about competition from MSFT, the market opportunity is too big to only for only one to thrive. Okta’s being a cloud-neutral platform with 7K integration is also a strong selling point to enterprises. This is especially true when smaller vendors are distracted as they move to the cloud. The management guided 16-17% Rev growth for FY24 Rev growth compared to 40%+ this year. The short-term number is likely derisked and the Long-term outlook is favorable after the acquisition of Auth0.

III: Inflection Point on Efficiency

From a margin and FCF perspective, the company has hit an inflection point. OPM turned from 0% to 9% in the most recent quarter as the Management focused on profitability through RIF and efficiency management. Similarly, the FCF margin improved from 1% to 14%. We think there is further upside from S&M and R&D in the medium term as integration improves with Auth0.

On growth outlook and valuation, FY24 revenue guidance of 16% is a significant slowdown from FY23’s 43%, which seems conservative with room for outperforming. Our model base case underwrites a 26% CAGR over the next three years ($1.9B to $3.8B) and significant improvement for FCF margin from LSD to high teens. As a reference point, Okta guided for $4B revenue and 20% FCF margin in FY26 before the integration situation blew up.

Key Catalyst for FY24 / CY23 and FY25: 1) stabilizing trend in CIAM through the acquisition of Auth0 2) Continuous expansion into adjacent markets through IGA and PAM products. 3) Ongoing Sales leadership search. 4) Greater expansion in the international market (currently around 20% revenue), 5) legacy replacement that could be gaining momentum post-COVID. 6) OpenAI as a strong push for customer awareness and help increase market share in CIAM

Chart of the Week in the Public Market:

It has been a week of a rollercoaster ride with FOMC meeting and the constantly evolving US banking crisis. Fed hikes rate by 25bps, which brings federal-funds rate to 4.75%-5%. The Fed’s move is consistent with the market consensus that inflation is the bigger priority for the Fed. Stock initially rose but soon gave up all the previous gains when Powell made it clear that there won’t be a pivot this year. Yellen also rains on Powell’s parade by stating that the Treasury officials had no intention to expand federal insurance to all US banks, at least as of now. Stock sold off on Friday.

Fed policy, Inflation Rate, and the Credit Suisse event continue to be the spotlight for this week’s sector-based focuses. Despite in-week volatility, the overall Fintech index remained stable from 7.7x to 7.6x - Consumer Fintech continues to lead up the pack with recovery while B2B payments saw muted performance.

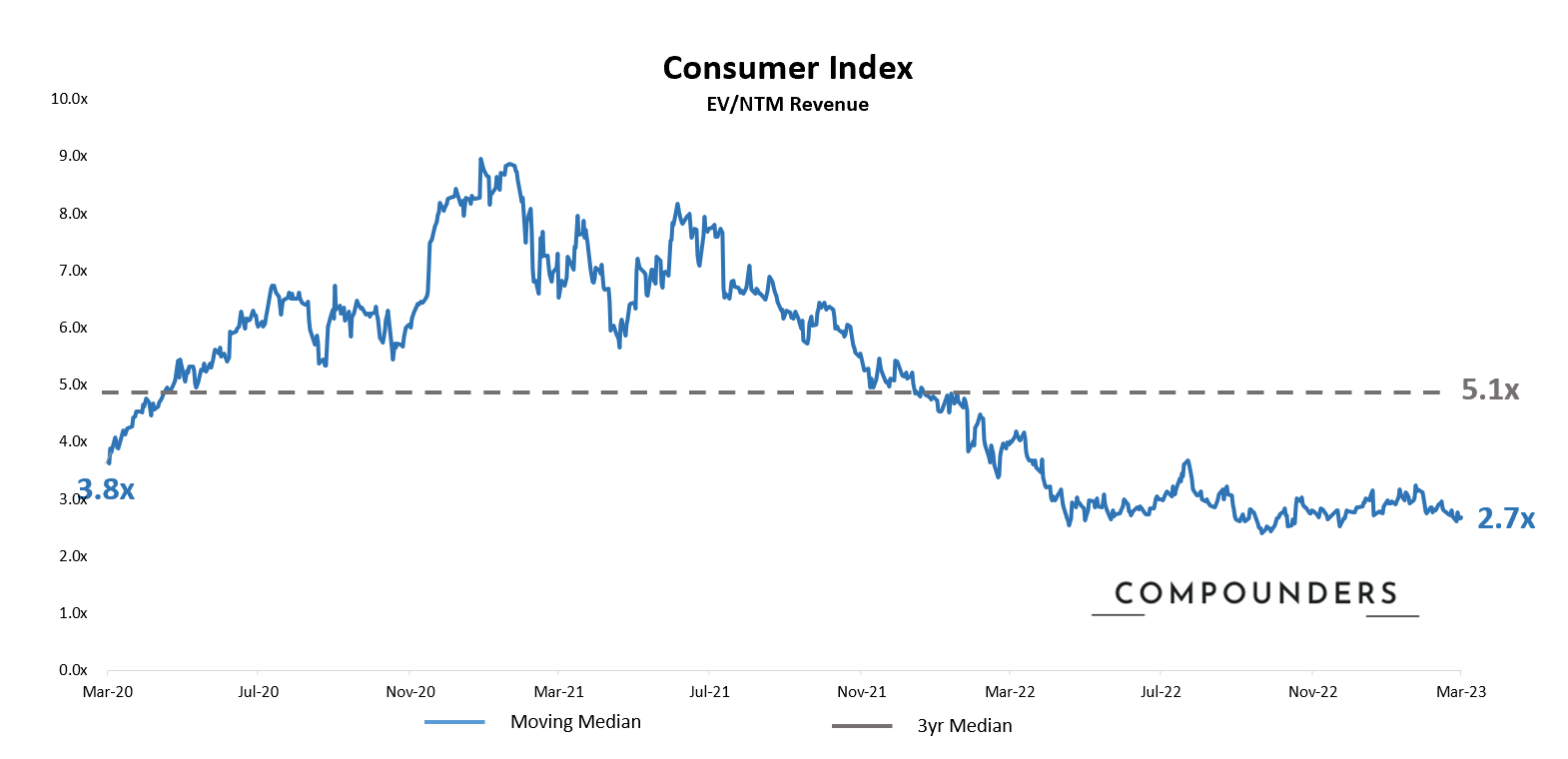

Index continues to be stable at 2.7x - no major changes in the subsector performance either, with Gaming climbing slightly up from 4.6x to 4.7x.

(Market data as of 3/23/2023, source: Bloomberg, CapIQ. See index composition at the bottom)

Chart of the Week in Private Market

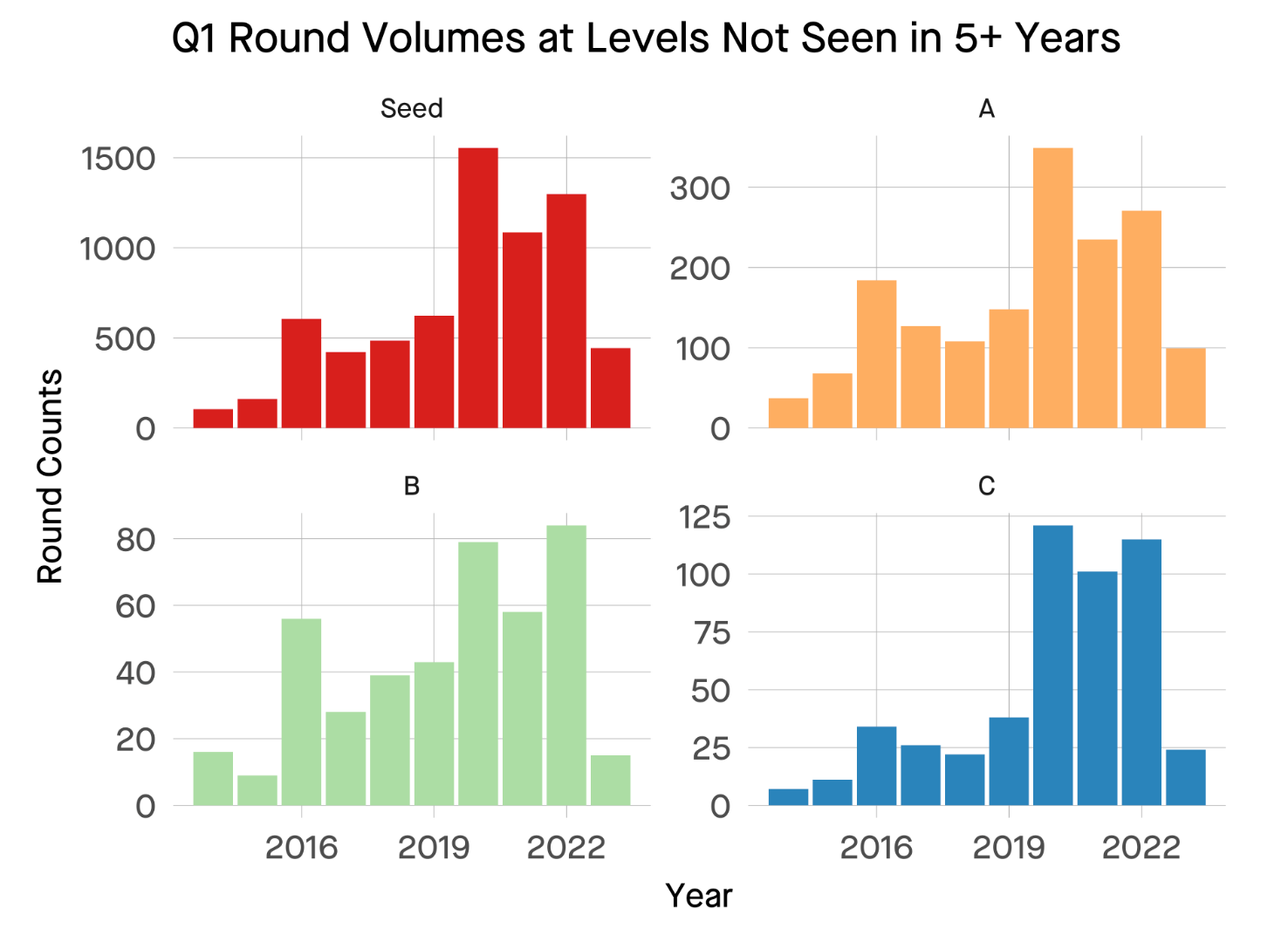

After the Stripe announcement, the private landscape went back to a more muted environment. No major growth announcement with over $100M fundraise amount. The index will trail high for 2 more weeks as we do a 1 month trailing but expect norm revision right after that. Tomasz’ blog also showed our index chart in a stage-focused way for Q1 YoY comparison. Continued to be impressed by the quality of his blog and recommends folks a read.

(Deal data as of 3/26/2022, source: Pitchbook. Defined as - Series B+ global growth stage deals)

Sources: Software Index: over 200+ public companies / Fintech Index: V, MA, PYPL, SQ, BILL, ADYEN, SHOP, LSPD / Consumer Index: ABNB, BMBL, CHWY, CVNA, DASH, DHER, DKNG, DUOL, ETSY, FB, FTCH, GDRX, GOOGL, MTCH, NFLX, OPEN, PINS, POSH, PTON, ROKU, SFIX, SNAP, SPOT, UBER, W. Please feel free to ping us for further detailed breakdown