Compounders 11.13.22

To stay in touch, you can find us here: GZ's Twitter and Shan’s Twitter

Bear Market Rally: Let’s Break it Down

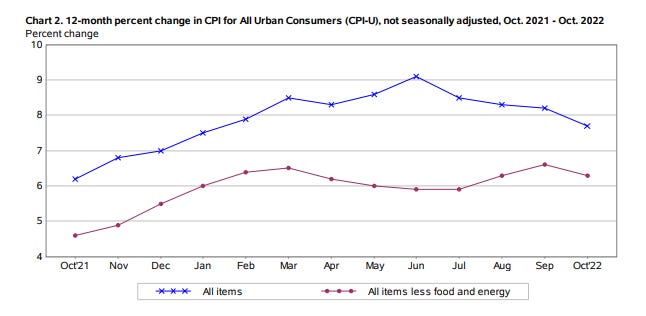

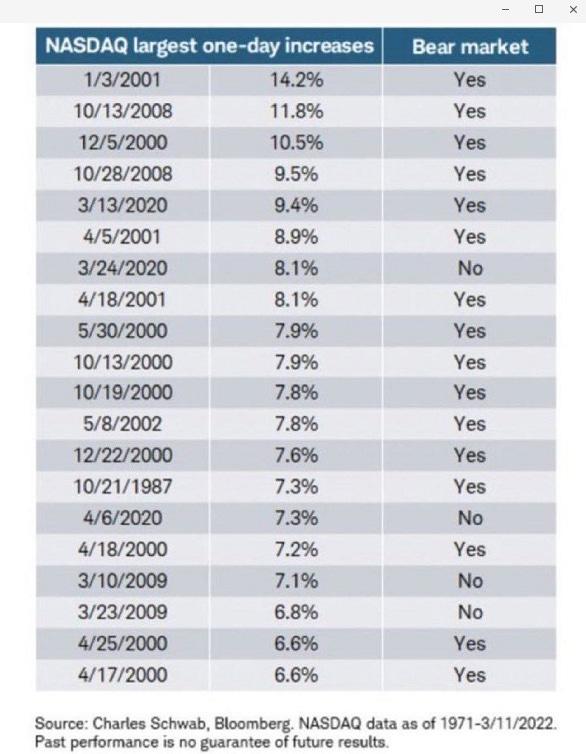

It has been a turmoil week for many, so we will keep it short. CPI is finally trending towards the right direction, rising 7.7% Y/Y and below expectation. Core CPI also came in below the expectation at 6.3% annually. Tech enjoyed its best two days over the past two years. A strong rally might look strange in a bear market initially, but it is not that uncommon in history. See below for the most significant daily movements in Nasdaq, and one will soon notice that many strongest rallies happened in the bear market! When the market sentiment gets squeezed to the extreme, some good news can catalyze a sweet rebound. CPI serves as a short-term catalyst for a long-overdue recovery. We believe a few reasons drive this round of the tech rally:

Mega tech start to lower the guide

SMID somewhat de-risked after a dramatic gap down in the round of earnings

Inflation peak and Fed slight pivot

Geopolitical tension relief

The market is getting used to high yield. The path is more predictable.

Sentiment suddenly changed from “inflation shock, rates shock, recession shock” to “Peak CPI, peak Fed, Peak yields, peak US dollar”. You can’t go wrong by playing along.

What is next? We next the market rally to continue until macro data like Non-farm payroll comes out or Q4 earnings wake up the bear, and then we might finally be ready to capitulate to reality.

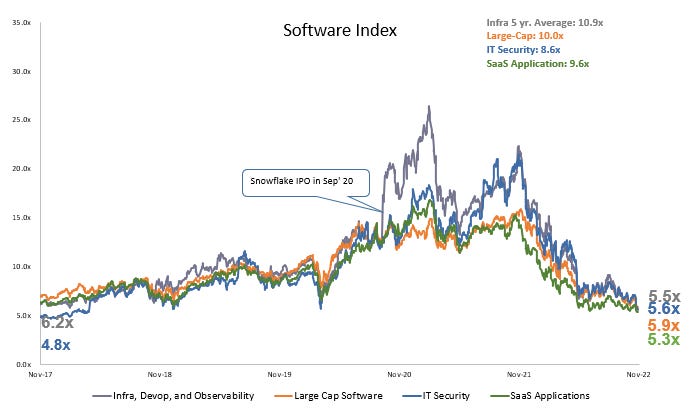

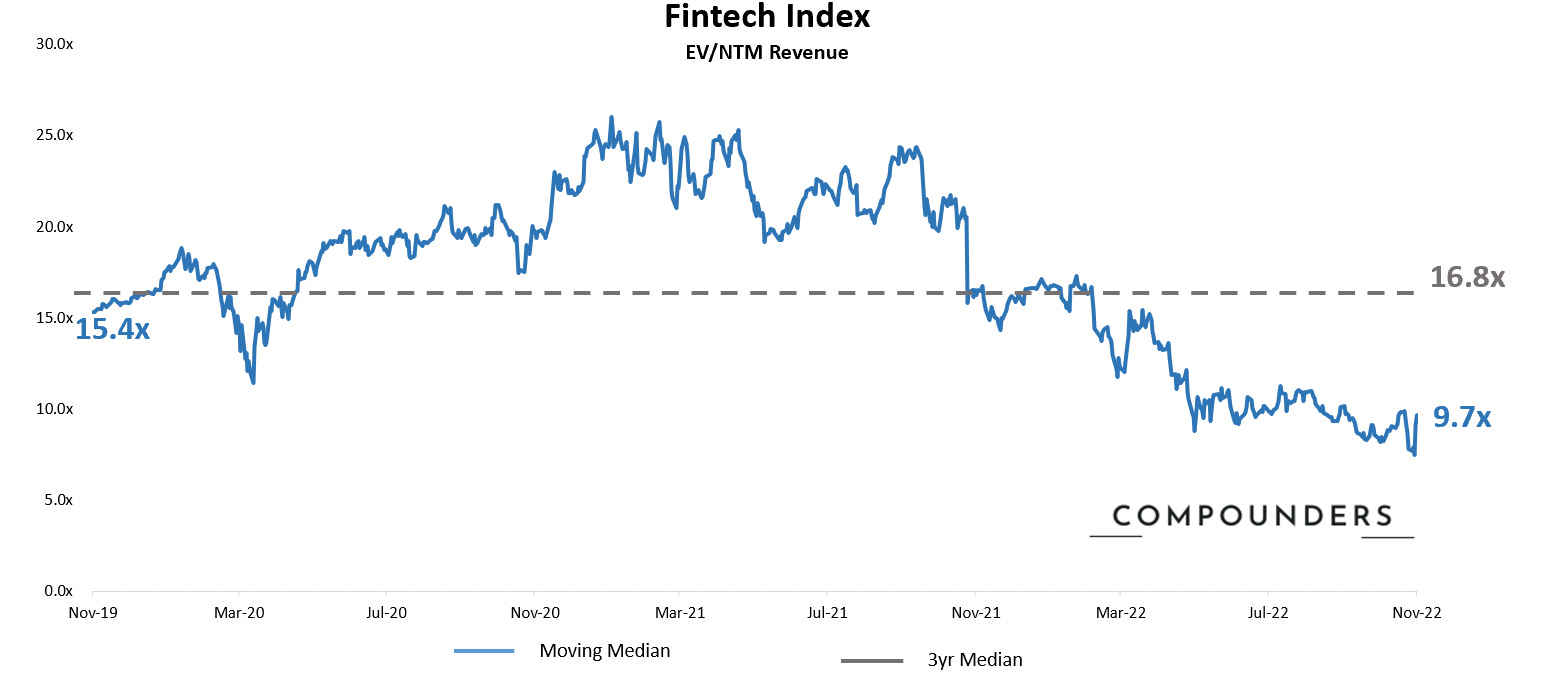

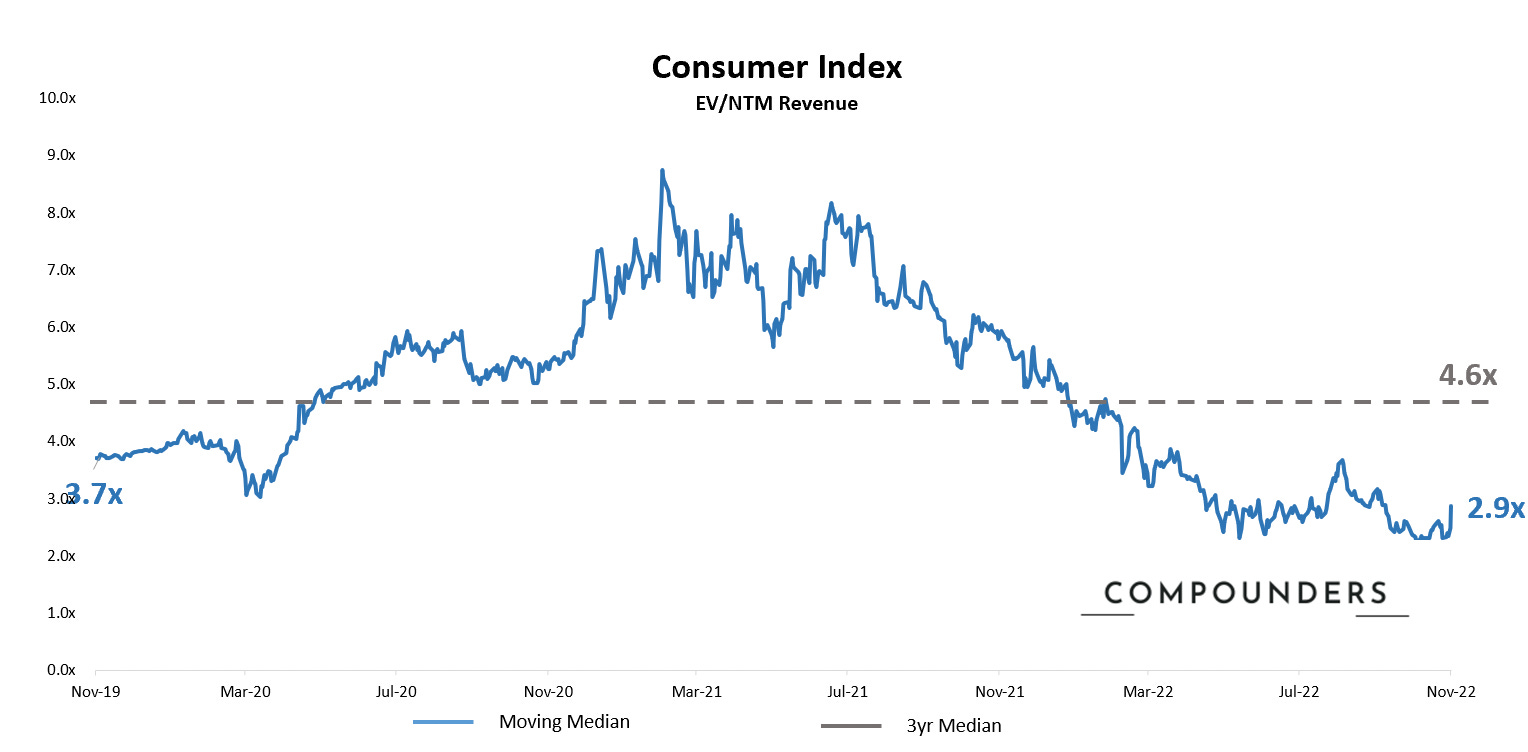

Chart of the Week in the Public Market

Strong rebound across the tech industry driven by a better-than-expected CPI print.

Quick bounce back from last week’s all-time low - Index dropped to just 8x last week and now has recovered to 9.7x. CPI print lifted the whole market and positively impacted the fintech sector alike.

Similar rebound like all other sectors - from last week’s new low of 2.3x to 2.9x.

(Market data as of 11/11/2022, source: Bloomberg, CapIQ. See index composition at the bottom)

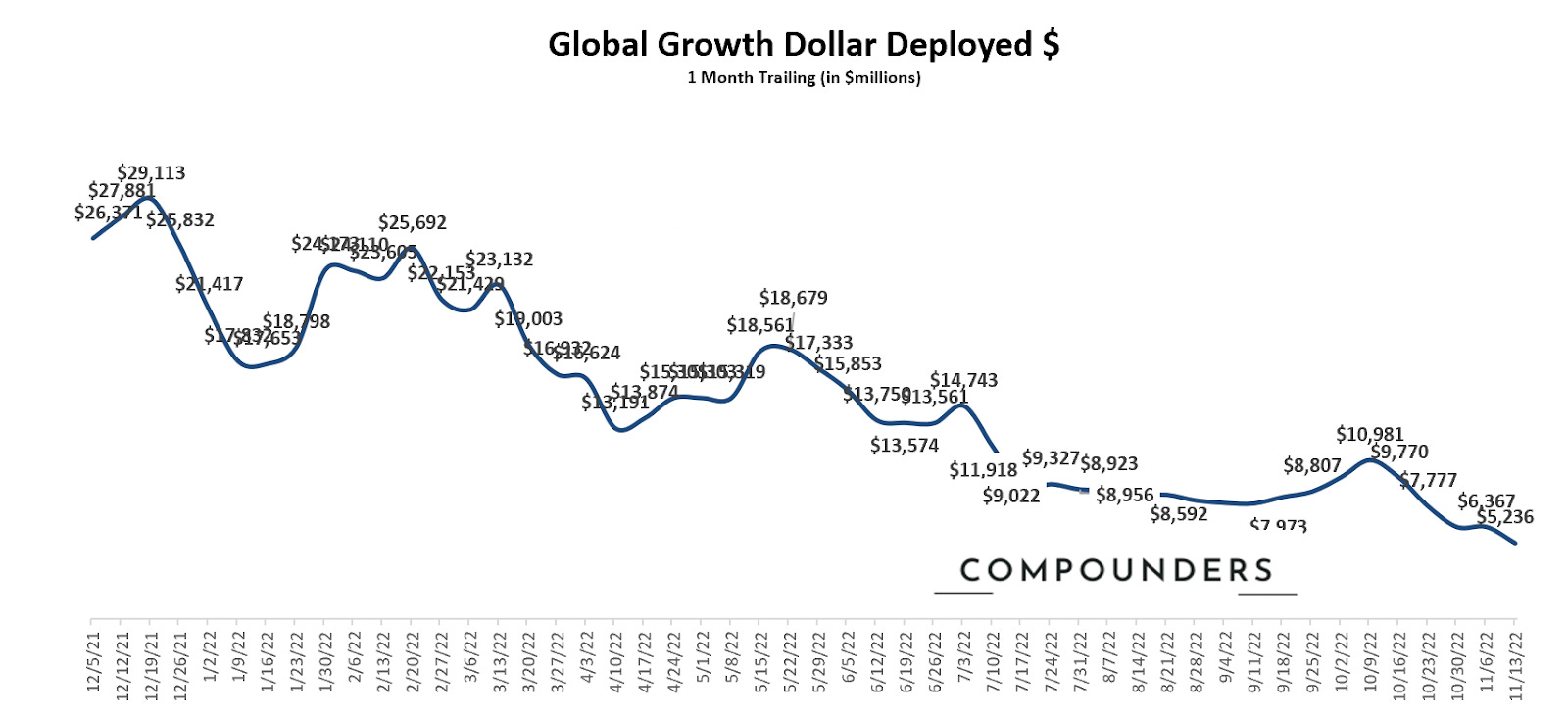

Chart of the Week in Private Market

(Deal data as of 11/13/2022, source: Pitchbook. Defined as - Series B+ global growth stage deals)

New Low - now it officially does not seem like the rebound coming out of summer would be long-lived. Capital still predominantly remains on the sideline. This could be a rough winter.

Sources: Software Index: over 200+ public companies / Fintech Index: V, MA, PYPL, SQ, BILL, ADYEN, SHOP, LSPD / Consumer Index: ABNB, BMBL, CHWY, CVNA, DASH, DHER, DKNG, DUOL, ETSY, FB, FTCH, GDRX, GOOGL, MTCH, NFLX, OPEN, PINS, POSH, PTON, ROKU, SFIX, SNAP, SPOT, UBER, W. Please feel free to ping us for further detailed breakdown