Compounders 2.13.22

To stay in touch, you can find us here: GZ's Twitter and Shan’s Twitter

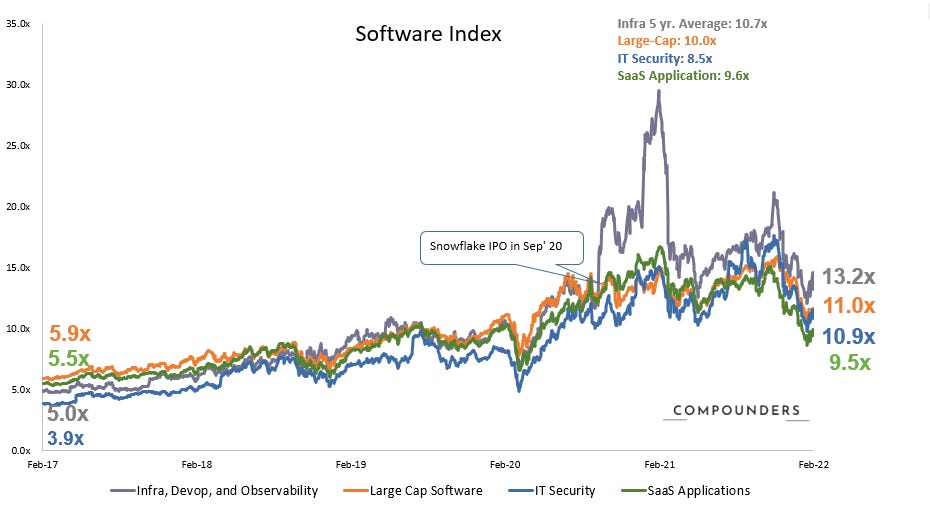

Chart of the Week in the Public Market

Software multiples contracted following a worse than expected CPI data and escalating tensions between Ukraine and Russia. For the first time in 40 years, inflation went up to 7.5%, which led to the 50bps rates hike fear again. Following a subdued risk appetite, all subsectors moderated slightly. Infrastructure software valuation continues to lead the pack.

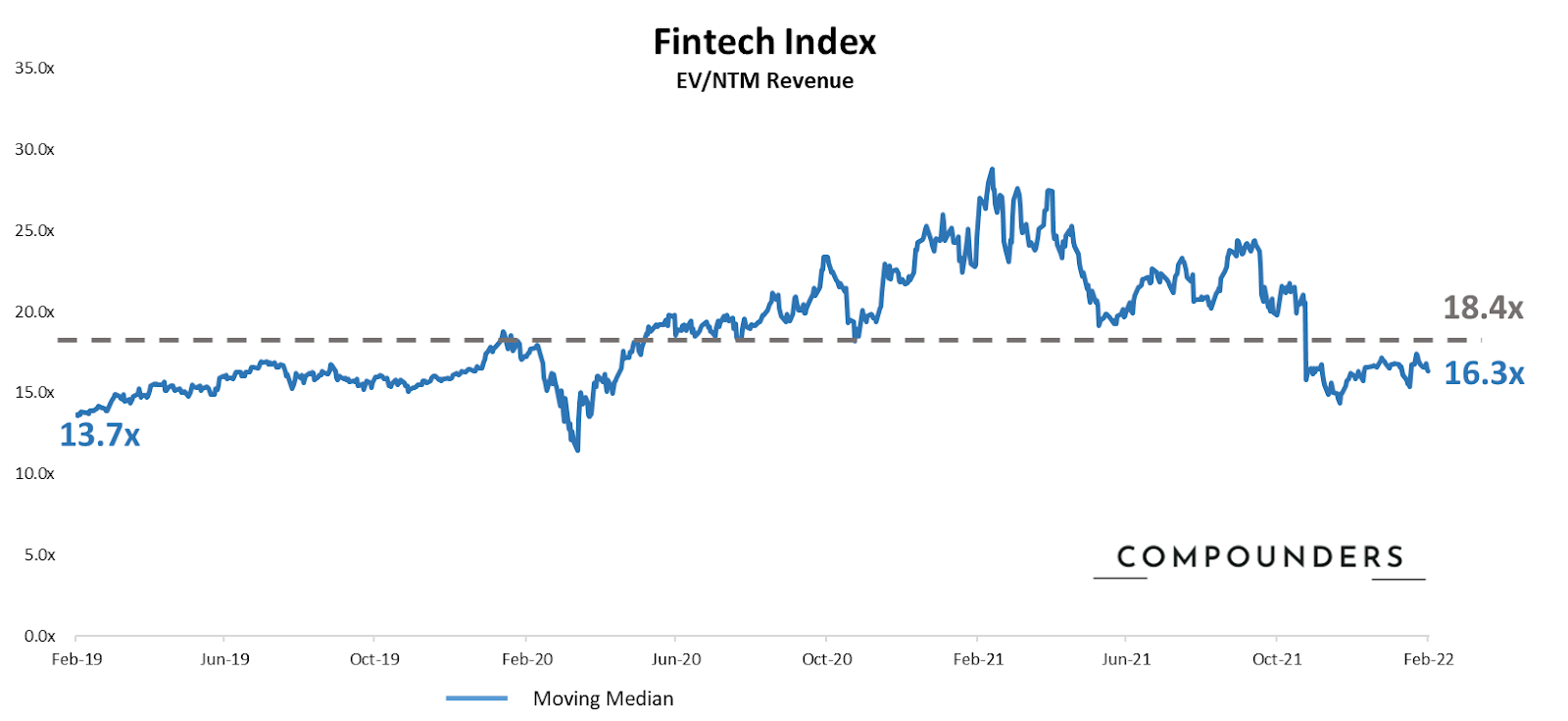

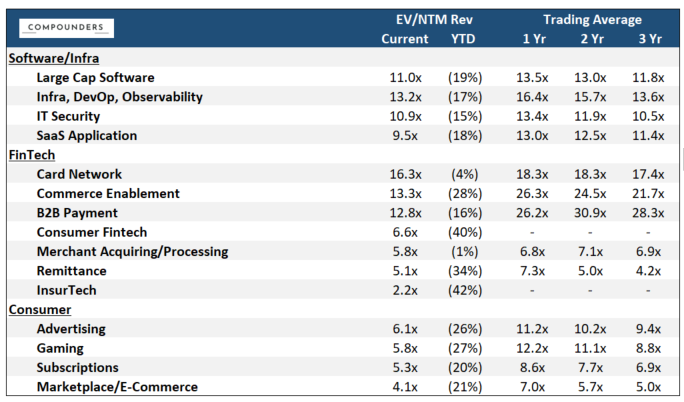

Fintech Index EV/Fwd Rev multiple decelerated from 17.3x to 16.3x and below 3yr median 18.4x. BILL moderate after last week’s jump. Merchant acquiring/processing giants FISV and GPN reported this week with in-line results.

Consumer Index EV/Fwd Rev multiple moderated from 4.7x to 4.6x during last week, below 3 year median 5.8x. Uber investor day was the main event in the sector this week - LT bookings guidance of 22-25% was in-line with the street but outlook of 3% margins in 2024 may have slightly underwhelmed investors.

(market data as of 2/11/2022, source: Bloomberg, CapIQ. See index composition at the bottom)

Public Market Commentary:

A heavy week of software earnings, but we walked out feeling better about high-quality growth companies than ever. Under the backdrop of rising interest rates and a hawkish Fed, the market prefers assets with improving margins, efficient GTM and sustainable cash flow. In a slowing economy, growth becomes a scarcity for investors. That's why we believe high-quality growth companies will continue to command premium valuation. The market diverges on this week's earnings: Datadog's stock bounced back to November's high following a monster quarter with record growth and steady margins, while cash-burning Confluent sold off 30% in two days. High-level recap from last week:

Datadog: The king delivers another record quarter

Datadog never ceases to amaze us with its extraordinary execution. While its two competitors, Dynatrace and New Relic, both sold off heavily following revenue deceleration and light guidance, $DDOG delivered 84% YoY revenue growth with record net new ARR and new logos adds. It’s worth calling out that it achieved sustainable growth with cash efficiency (cash up 20% Y/Y). The stock up 17% AH, approaching the 2021 November high.

Confluent: Open source sweetheart missed expectation

Confluent, a hypergrowth company, suffered from expectation miss despite revenue acceleration. Revenue was up 71% YoY but still seems light given high buy-side expectations. Cloud revenue decelerated to 211% vs 245% in the previous quarter. We don't see the company turning profitable any time soon, with S&M growing at 70% revenue and R&D 30% of revenue. The current market condition can be unforgiving when it comes to revenue deceleration in premium multiple stocks. The stock was down 10% AH and retreated another 25% on the following day.

Cloudflare: Long-term story intact but valuation reflects premium

Cloudflare is another “story stock” that comes with a lot of volatility. Its premium valuation was supported by a series of edge computing and zero-trust security initiatives. The company reported an accelerating revenue growth of 54%, supported by strong enterprise momentum and large customer adds. The market is happy to see product initiatives like Cloudflare Workers progress in the right direction. However, its higher CAPEX intensity in 1H22 will push cash flow down to the negative zone. While we remain optimistic about its leading position in edge computing, the company will likely face much pressure due to its premium valuation and cash burning profile.

Software Earnings Biggest Takeaway: Long Software! We are now three weeks into tech earnings - most companies' results came out stronger than expected with no signs of pull forward demand. Software is still better positioned than many other tech sectors, supported by its strong fundamentals and relative muted impacts from COVID and supply chain issues.

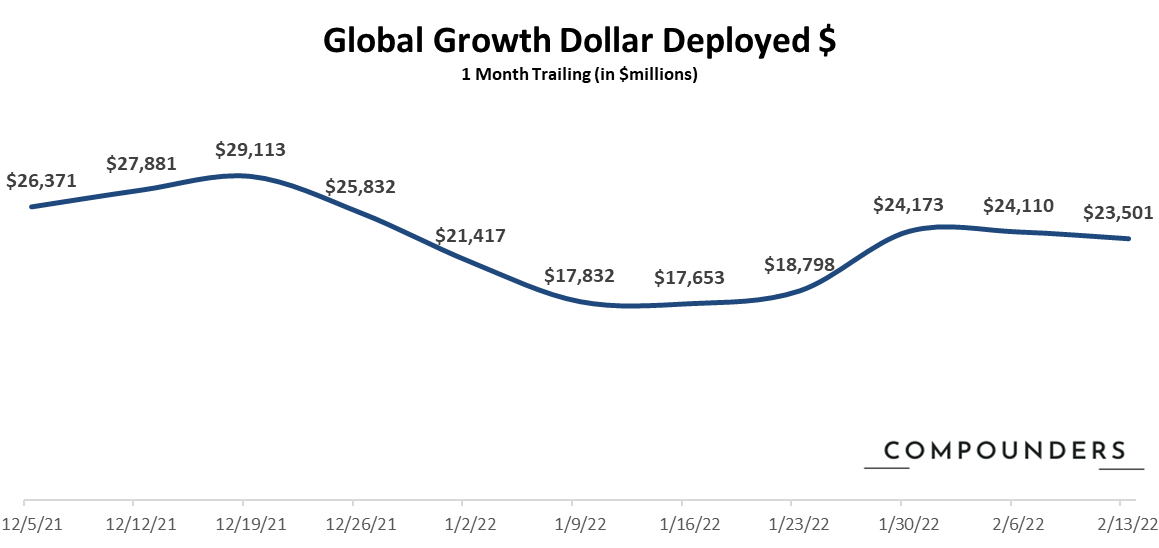

Chart of the Week in Private Market

(Deal data as of 02/13/2022, source: Pitchbook. Defined as - Series B+ global growth stage deals)

Private Market Commentary:

This week saw a slight moderation of global private deals announcement and growth dollars deployed. The latest 1 month trailing data point would imply that the Jan deployment velocity hasn’t seen major acceleration after holiday lows. Some fundraising/business announcements we are watching this week are (note: valuation in post-money unless otherwise specified):

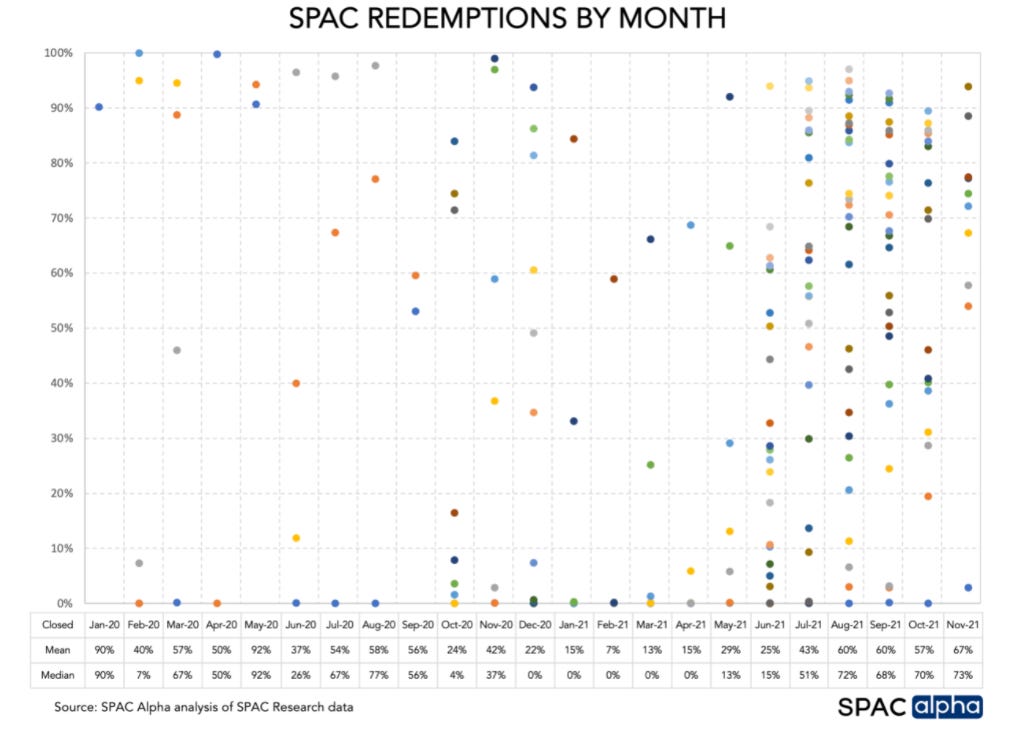

1. SPAC - who stopped the music? No one could have walked out of the public/private market in 2021 without hearing the word SPAC. According to EY IPO research (source), 150 out of the 400 private companies that went public on the U.S. stock exchange by mid-Dec 2021 are blank check companies. This week’s TermSheet commentaries really draw our attention to some of the recent momentum reversal. Kin Insurance pulled the plug on a deal to go public via SPAC merger (source). Earlier in the month, consumer fintech startup Acorns also walked away from the $2.2 billion SPAC merger with the plan to raise additional funding from the private market. So:

What happened? The underperformance of de-SPAC stocks is certainly a major contributing factor. But digging beyond the surface, we found that there has been a significant change in one important underlying metrics - Redemption Rate (investors’ right to redeem shares at the IPO price before a merger is official). From Jan-July, 2021 the average month SPAC redemption rate ranged from 7-43% vs. the number jumped to 43-67% in July-November. Mean redemption rate jumped from 15% in Jan-21 to 67% in Nov-21. If a large percentage of redemption rate is exercised, then the combined company may face reduced cash proceeds for future operations. While it’s hard to pinpoint the rising redemption rate to one particular reason, SEC’s recent probes into several high-profile SPACs as well as investors’ subdued risk appetite for companies in speculative industries may have contributed to this. There are of course many ways to prevent this from happening but the potential implication of redemption still may bring additional worries and risks to the consideration of SPACs. (Reuters has more here)

2. Crypto - From Good to Have to Must Have: This week, Robo advisory firm Betterment announced the acquisition of Makara, a cryptocurrency portfolio manager. Betterment plans to leverage this acquisition to provide consumers and financial advisors the ability to invest in expert-built, diversified crypto portfolios alongside existing investments. Betterment CEO stated in an interview that “Crypto is here to stay and Betterment wants to live our promises of long-term diversification and to provide our customers with the best variety of assets in the marketplace…”. Increasingly, we have observed consumer fintech players bring up the priority of crypto product offerings in their roadmap either through acquisition or build-outs. Our 1/30 issue briefly discussed why GZ and I are bullish about the long-term prospect of the blockchain ecosystem. This undeniable wave of end users adoption will further drive crypto as an asset class from a “good-to-have” to “must-have”.

3. Valuation, valuation, valuation: Pitchbook published its annual U.S. VC Valuation report (source). 2021 again marked a record year for the industry with valuation jumps at an unprecedented magnitude. Early-stage valuation (Series A/B) saw a 50% yoy jump to $45M median pre-money valuation. Top percentile deals are done at almost a 2x rate of $100M. Late-stage companies saw an average valuation step-up of 2.9x between rounds. Growing along with the valuation ste-up is the VC exit liquidity - rolling four-quarter median VC step-ups at exit reached a new high of 1.7x - highest value since 2012. But given the recent public market volatility, we would be curious to understand how that may impact potential step-up multiples for VC exits and hence larger considerations into valuations in the future.

Sources: Software Index: over 200+ public companies / Fintech Index: V,MA,PYPL,SQ,BILL,ADYEN,SHOP,LSPD / Consumer Index: ABNB, BMBL, CHWY, CVNA, DASH, DHER, DKNG, DUOL, ETSY, FB, FTCH, GDRX, GOOGL, MTCH, NFLX, OPEN, PINS, POSH, PTON, ROKU, SFIX, SNAP, SPOT, UBER, W. Please feel free to ping us for further detailed breakdown