Compounders #46 Warm or Cold Christmas? Quick take on Tech Jobs and China Reopen

Compounders #46 Warm or Cold Christmas? Quick take on Tech Jobs and China Reopen

12/11/22

To stay in touch, you can find us here: GZ's Twitter and Shan’s Twitter

Warm or Cold Christmas? Quick take on Tech Jobs and China Reopen

December is my favorite time in NYC when the whole city get festive with Xmas tree decorations. It’s hard not to get hopeful about life when you hear bell jingles and see people sipping on hot chocolate on a crisp Sunday morning. Yes, we are so ready to move past a crazy year. Many of us are battling year-end wrap-ups, so we plan to keep this issue short and sweet by highlighting key trends in tech jobs and China Reopen

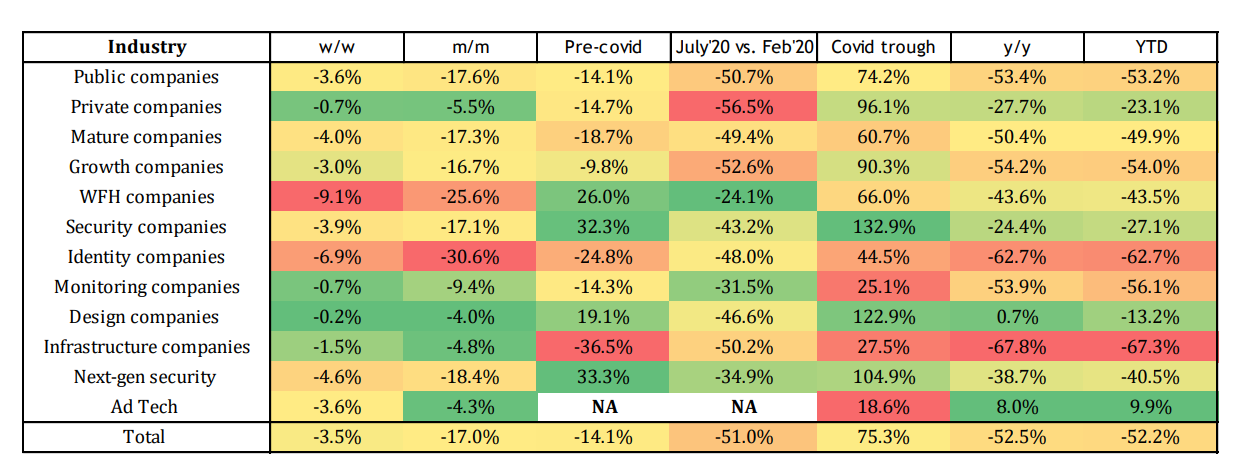

1. Tech Job postings down more than 50% YTD

The job market in tech continues to worsen as job postings down 8 months straight since March. To put data into context, July software job postings were down -10% Y/Y and -23% YTD vs. now down -52.5% Y/Y and -52% YTD. Despite the drastic decline, We haven’t seen signs of stablization yet as management prioritize cash burn/margin over growth.

How does it compare to the pandemic? The decline is a lot worse than COVID on an absolute basis. Based on data collected by RBC, currently, the tech job market is down 28,085 vs. down 4,922 over the same period in 2020. The decline during COVID was followed by a V shape recovery in 2H20, but this round of pain feels longer and deeper. While the tech job market cools down quickly, the broader labor market remains tight, as seen from non-farm payroll data. Traditional sectors like retail, travel and leisure are in better places than COVID.

Any vertical better off than others? Infrastructure saw the most decline (-67%) vs ad tech companies growing at 9.9%. Design companies and security companies held up relatively well as well.

Public vs. Private? Public companies scale back meaningfully (-53%) vs. private (-27%). Not surprising as public companies face more scrutiny from investors. We also know there’s a lag between public and companies’ performance as well as mgmt. decision timeline. Therefore, it wouldn’t be a surprise if private job posting comes into more of a halt or further decline in the near future.

(source: RBC capital markets)

2. China Reopen- From Zero COVID to lots of COVID

China’s reopening is a big topic with wide implications for the world order and geopolitical debate. We think tracking some key development over a series of posts is worthwhile as the situation unfolds. Kicking off the series with a post on Zero Covid Policy Pivot.

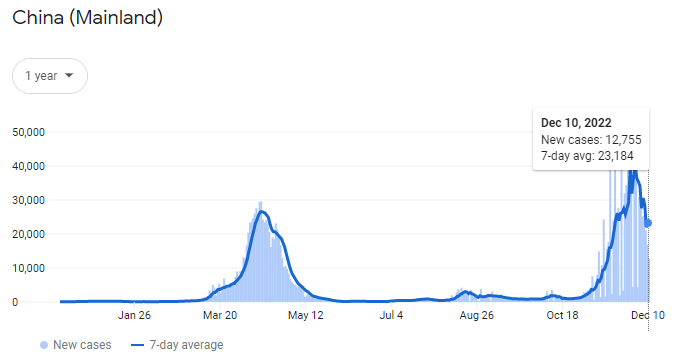

What happened? Last week, the Chinese government lifted its draconian “zero covid” policy after a mass street protest across several major cities in China. While this is not complete lifting, it is a pivotal change in a costly policy that has paralyzed the economy. For the past years, severe lockdowns and quarantine have been required to prevent large-scale outbreaks, which has slowed down nearly all forms of economic activities, leading GDP to precipitate to a 3% level.

A lot of COVID before the curve flattens. It is not surprising to see a surge in new COVID cases given Omicron's highly transmissive nature and older people's relatively low vaccination rate. The wave of infection seems unvoidable as the former deputy director of the Chinese Center for Disease Control and Prevention Feng Zijian predicted, “60% of the population may be inflected in the first wave before the curve flattens; 80-90% of the population may eventually be infected”.

Sentiment recovers, shaping a year of outperformance in 2023. Following the ease of policy, the market showed major signs of recovery with Hang Seng Index jumping over 12% in two weeks and Northbound net inflow totalling over $3B USD in a week.

US / China economic war: quite messy. Taiwan Semiconductor Manufacturing Company (TSMC) is moving to the US, with an initial investment of $40B in Texas (source). Chip sanction has been a key chokepoint to the value chain as semiconductors play an increasingly important role in cloud computing, AI etc. The US is trying to regain its dominance in the field after its market share declined from 37% in 1990 to 12% in 2020. Biden administration now provides over $50B to help companies build semiconductors facilities. In the meantime, Xi shook hands with Saudi and pledged to purchase more oil with RMB. The deal is considered a pivot move to ensure China’s energy independence.

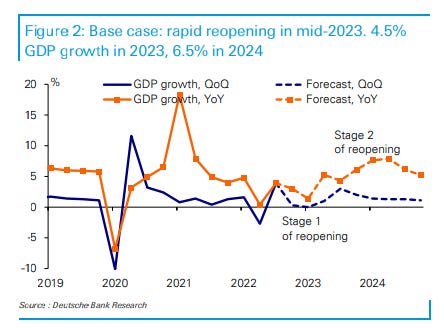

Path to economic recovery. We expect the recovery to be gradual, with the initial phase full of chaos: hospitals being busy with increased cases. Economic activities likely remain subdued given the virus. The public will gradually adjust psychologically and emotionally to fear. Based on what we have seen in the US, Q1 2023 will likely be driven by some pent-up demand in travel and offline services. GDP will normalize further as we head into Q2 2023.

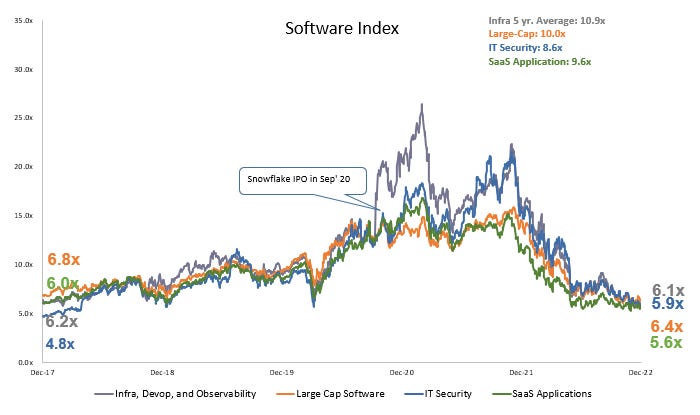

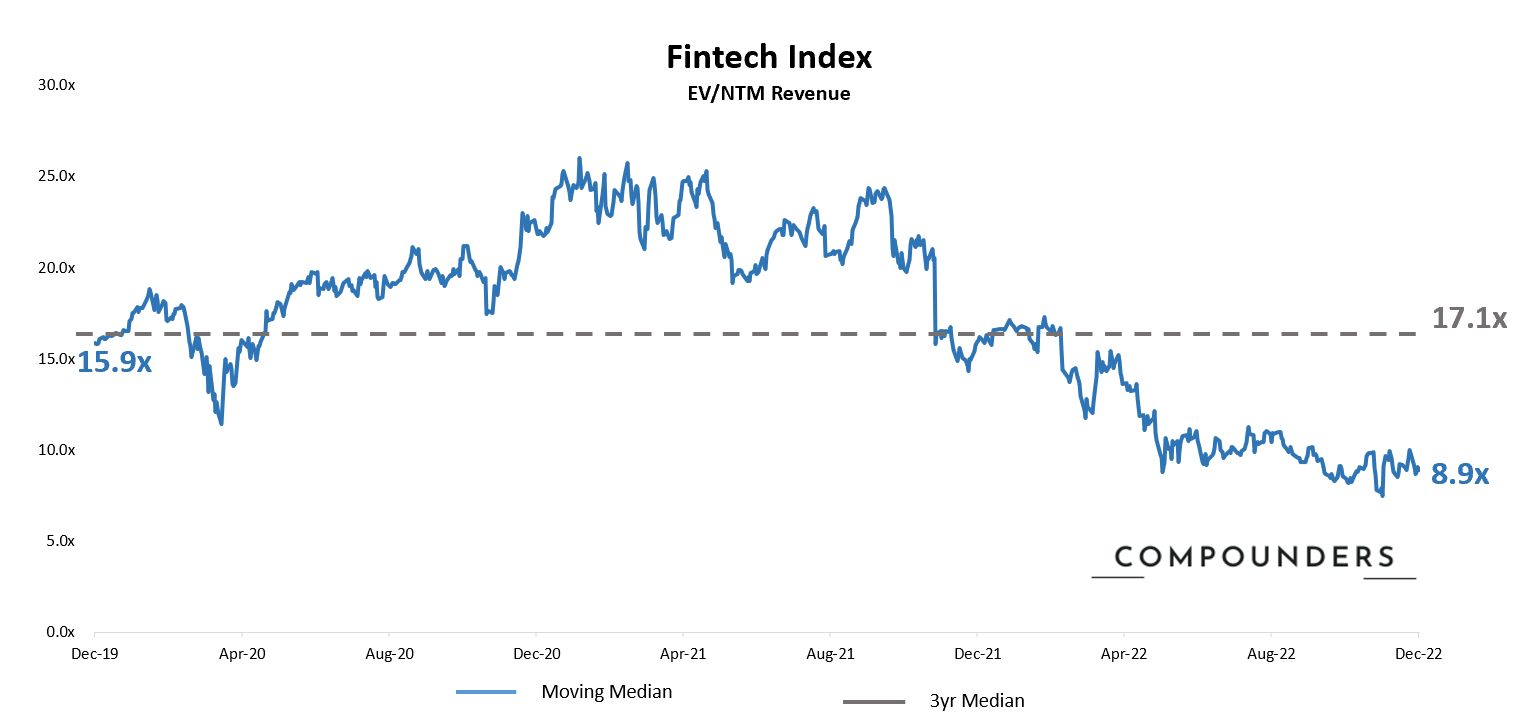

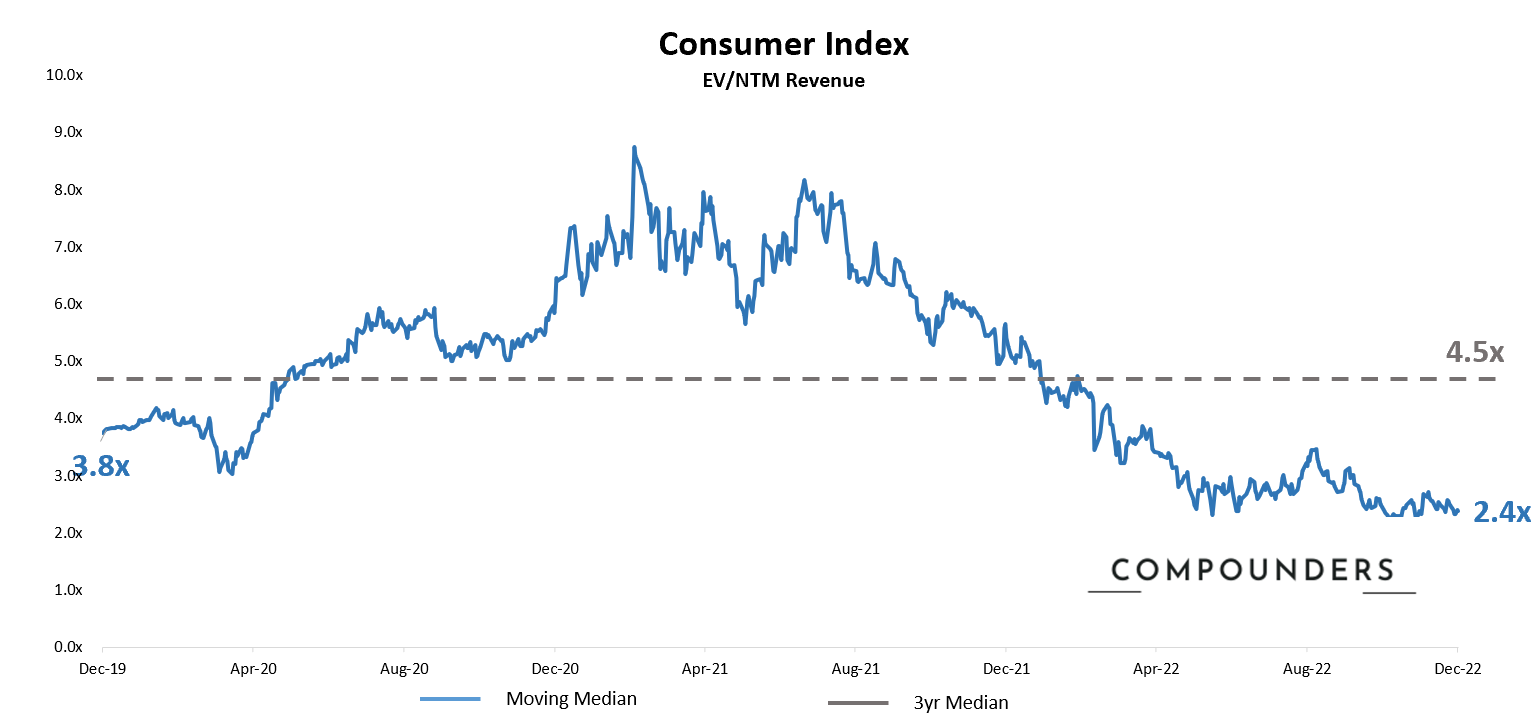

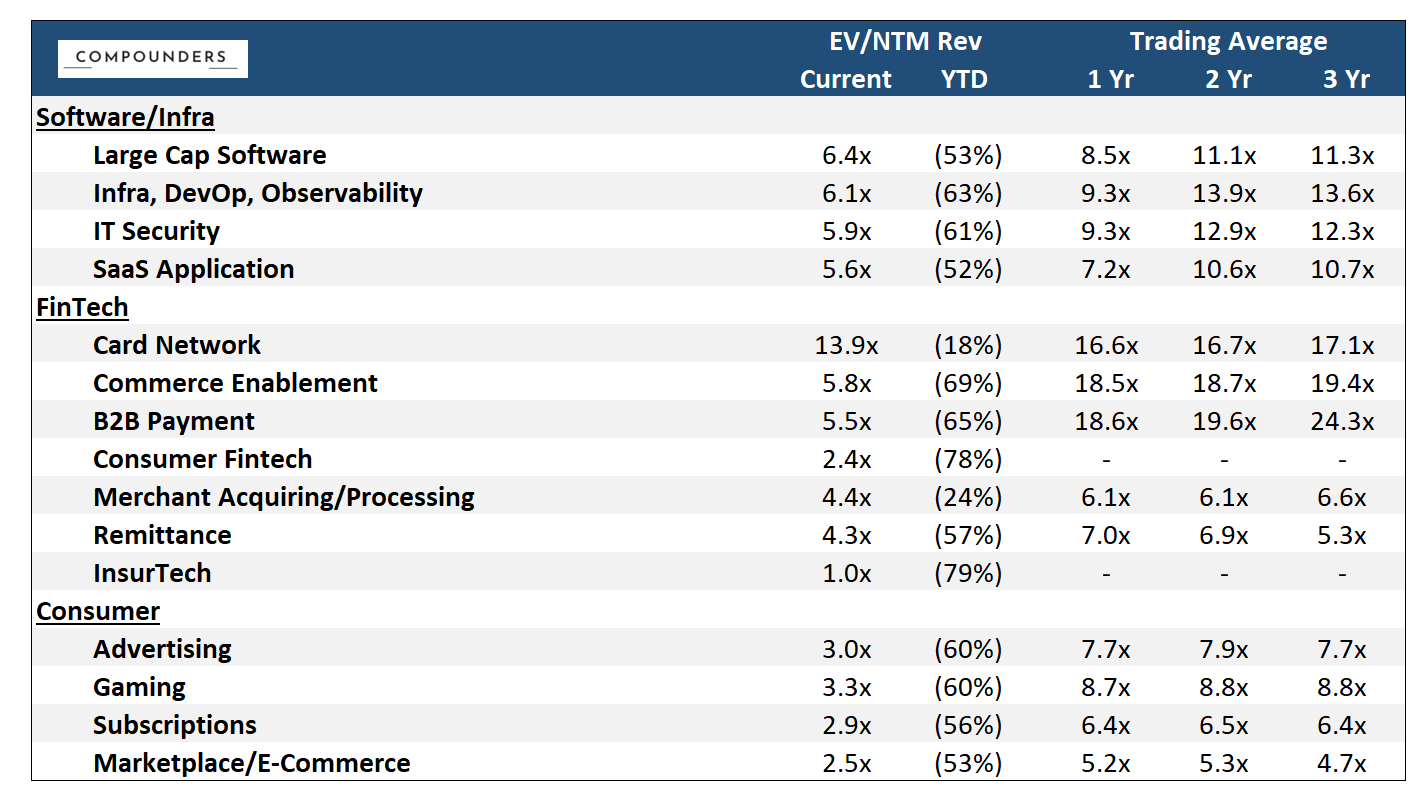

Chart of the Week in the Public Market

Market contracted slightly as a reversal to last week’s rebound. Strong PPI raised concern over inflation.

Small revision from last week’s 9.2x to 8.9x - two consecutive weeks of downward revision after a major rebound week. Among Fintech - InsurTech has been hit the most and is down -80% YTD. Card Network maintained its strength after the market rebound. Remittance also reverted back and held stronger than consumer fintech along.

Similar magnitude of revision with other sectors - down from last week’s 2.5x to 2.4x and two consecutive weeks’ of correction. Gaming has surpassed Advertising as the most highly valued sector vs. E-comm remains the most depressed.

(Market data as of 12/9/2022, source: Bloomberg, CapIQ. See index composition at the bottom)

Chart of the Week in Private Market

(Deal data as of 12/11/2022, source: Pitchbook. Defined as - Series B+ global growth stage deals)

Drata’s $200M and Einride’s $500M round drove the last week’s updated data slightly up. There were also increased activity in Asia (as a geo) and Healthtech (as an industry). But overall trendline seems to stay the same with small bounce back from time to time but overall trending down to ~$6B globally in the trailing 30 days basis. We continue to expect the year finishes with activities just about 25% of the same time last year.

Sources: Software Index: over 200+ public companies / Fintech Index: V, MA, PYPL, SQ, BILL, ADYEN, SHOP, LSPD / Consumer Index: ABNB, BMBL, CHWY, CVNA, DASH, DHER, DKNG, DUOL, ETSY, FB, FTCH, GDRX, GOOGL, MTCH, NFLX, OPEN, PINS, POSH, PTON, ROKU, SFIX, SNAP, SPOT, UBER, W. Please feel free to ping us for further detailed breakdown