Compounders 9.25.22

To stay in touch, you can find us here: GZ's Twitter and Shan’s Twitter

Market Commentary:

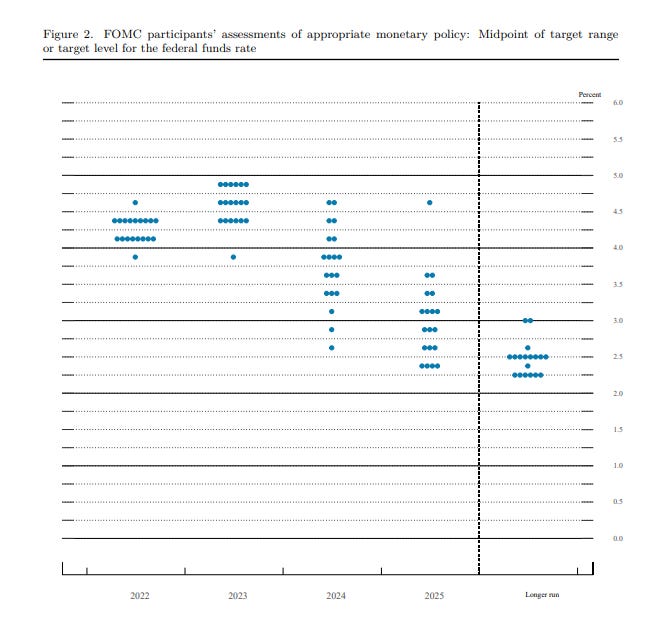

1.FOMC meeting - 75 bps and another leg down

The 75bps rate hike came in line with the market expectation & our prediction from the last edition. Powell made it clear that they were going to “keep at it.” They expect to see unemployment rise to 4.4% from 3.7%. This was a slap to the market that once believed the Fed would pivot sometime in 2023. The hawkish dot plot sends a simple message: they are willing to take more pain and is mentally prepared for it. No pivot in sight, at least for now. This sends the stock price back to June low and poses a greater question to investors: are you prepared for a 5% interest rate environment in 2023? (see dot plot for interest rate forecast below)

We think ultimately, it comes down to how fast does the inflation drop vs how much pain can the economy take? Under a soft landing case, inflation starts to fall more meaningfully and back to ~2% over the next 2-3 years. Under a hard landing case where the inflation is more sticky, the Fed would have to stay aggressive to push the interest rate above 5% and kill the economy.

Monetary policy is not a surgical knife and can't target which part of the economy to kill. The market fears that the Fed won’t stop until they break something. In our previous issue, we mentioned that the current valuation level prices in 3.5% 10yr TSY. But that level was quickly breached this week. Now we are at 3.687%, the highest level over the past decade. There is no surprise that “the other leg down” is coming. Sit tight. Things always get worse before they get better.

2. Compounders Thought Pieces into 2023, Part 1 - Looking Back to Look Forward

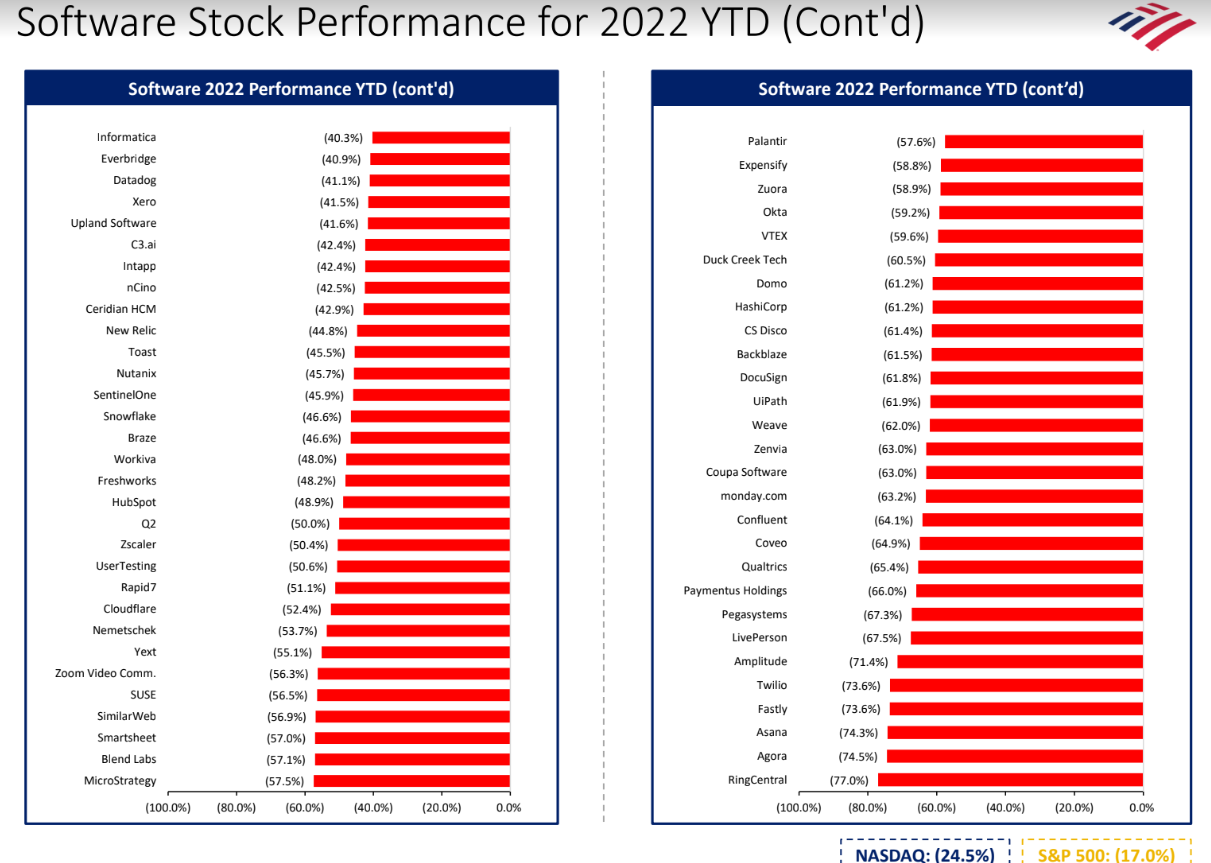

Now that we are sitting at the tail end of September and just 1 month away from Q3 earnings season, GZ and I find it only appropriate to prepare ourselves and think ahead into what could happen in 2023. This year has been nothing but volatile - to put things into perspective, some of the most well-loved stocks in the prior years got completely wiped out for 70-80% of their market caps. RingCentral -77%, Fastly/Twilio - 74%, Confluent -64%, UiPath - 62%, etc.. These numbers, plus changes in the macro environment that GZ has been educating our readers about, got us thinking - something more fundamental about the equity / asset valuation methodology has changed. It’s difficult to argue that these changes are for long and for good, but they will certainly impact us throughout this macro / fed cycle. As GZ stated in the prior section, as long as we are still in the continued rates hike cycle, it will be less likely to see any short-term rebound in 1) Consumer Confidence; 2) Labor Layoffs; 3) Asset Appreciation Rotation from Growth Profitability into Pure Growth.

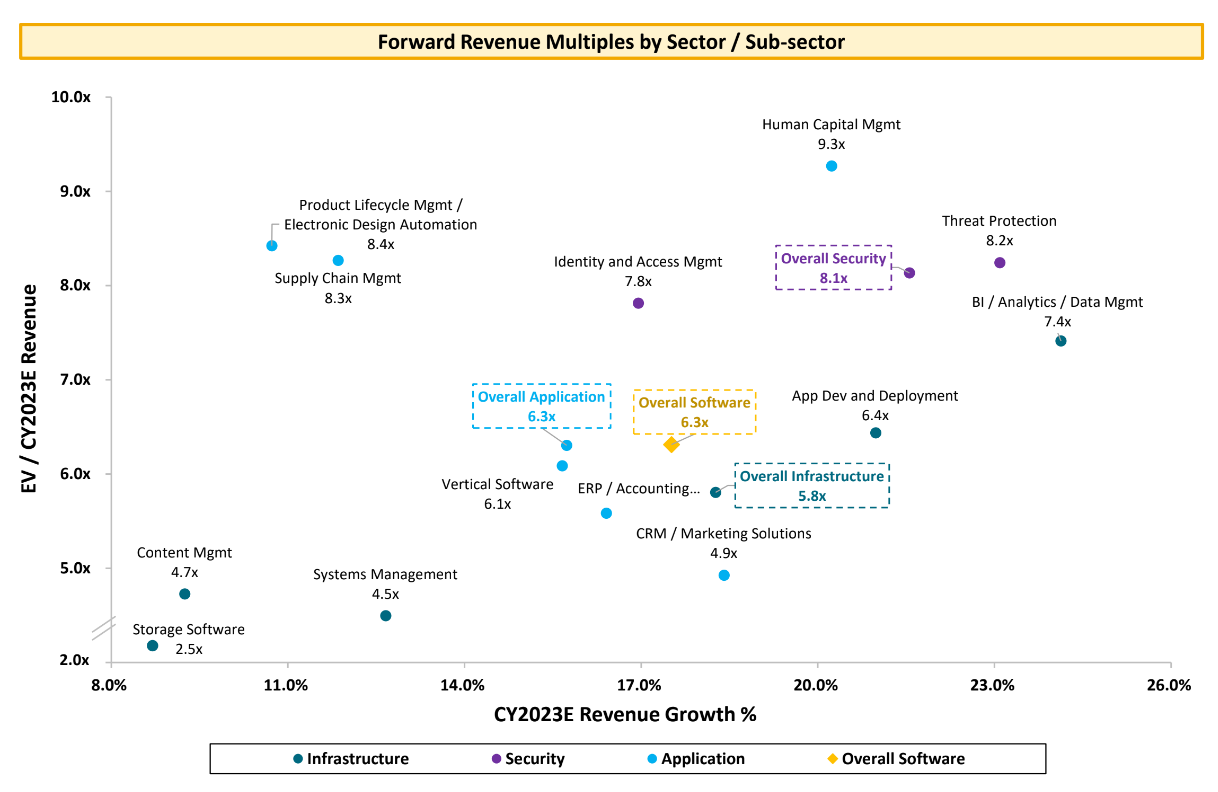

(source: BAML Software Sep Update)

So while the macrocycle is still in full swing - how should we anchor valuation and asset pricing? Ultimately, we are old-school and always prefer to return to DCF. Cash Flow Generation & Compounding Earnings Power, whether 5 or 10 years down the line, are how we see a company drives shareholder value. That being said, we also have become increasingly aware of the 1) thematic and sector-driven headwind-tailwind, and 2) relative defensive strength among different industries in a down market. Just think - when labour cuts start to impact business expenses, which part of the budget and contract will be dis-renewed first? I found the chart below from BAML’s latest software update really fascinating (huge shout out to that research team btw) - It’s clear to us that despite that most of the market return is driven by Beta factor at this point, there’s still a lot of bifurcation and sector-based alpha to be generated. For example, the implied growth expectation for 2023 FY is higher for Threat Protection / BI - Analytics and Overall Security. Those are also valued at the top half of valuation ranges. Despite higher growth expectations, however, CRM & Marketing solutions are lowered at the bottom quartile. Admittedly, this is taking a snapshot of a time and drawing conclusions on incomplete regression data points - but we still think these sub-sectors bifurcation imply where in the areas that could exist more potential for long-duration, high-efficient growth, compounding players over the long run.

GZ and I will continue to write about Reflection of 2022 + Thought Pieces into 2023 over the next 3 months. Stay tuned as we dive more into Themes of Choice + Macro Outlook + Fantastic Companies and Where to Find Them (Harry Potter fans i hope you get the reference ;)

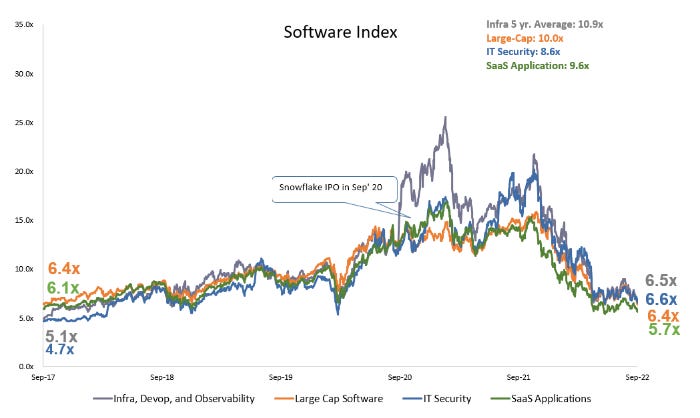

Chart of the Week in the Public Market

Massive selloff continues following the FOMC meeting. Infra fell from 7.1x to 6.5x. Security trades at 6.6x vs. 6.9x prior. Large Cap contracts from 6.9x to 6.4x, and SaaS application trades at 5.7x vs 6.0x prior.

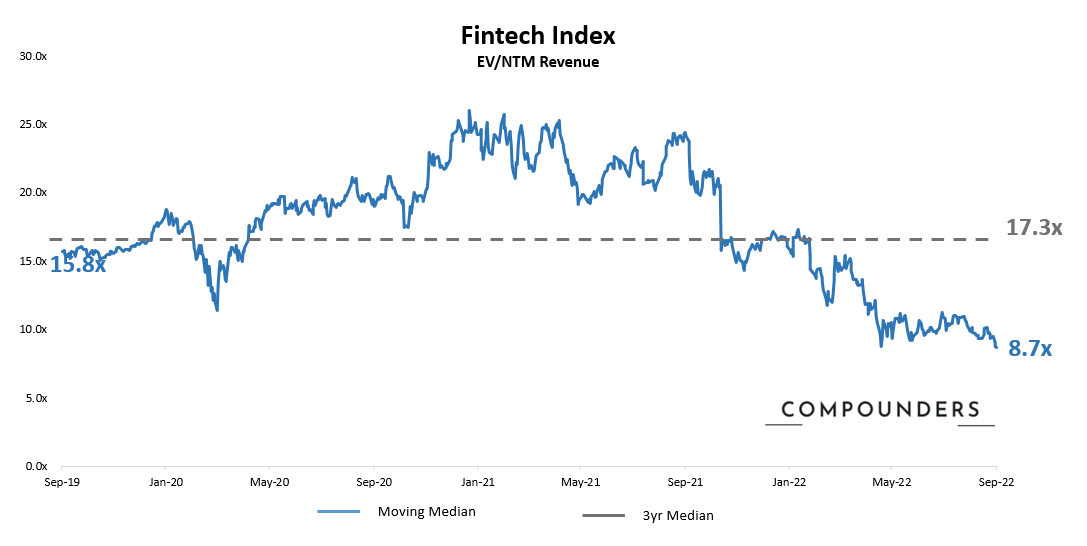

Total bloodbath in the market - Fintech sold off with the broader market to an all-time low point at 8.7x. Notably, this sector’s decline historically has been driven by Consumer Fintech / InsurTech etc. But those subsectors have actually stabilized at 60-70% down YTD while the Commerce Enablement and B2B Payment spaces drove bulk of the deterioration in the latest round of sell-off.

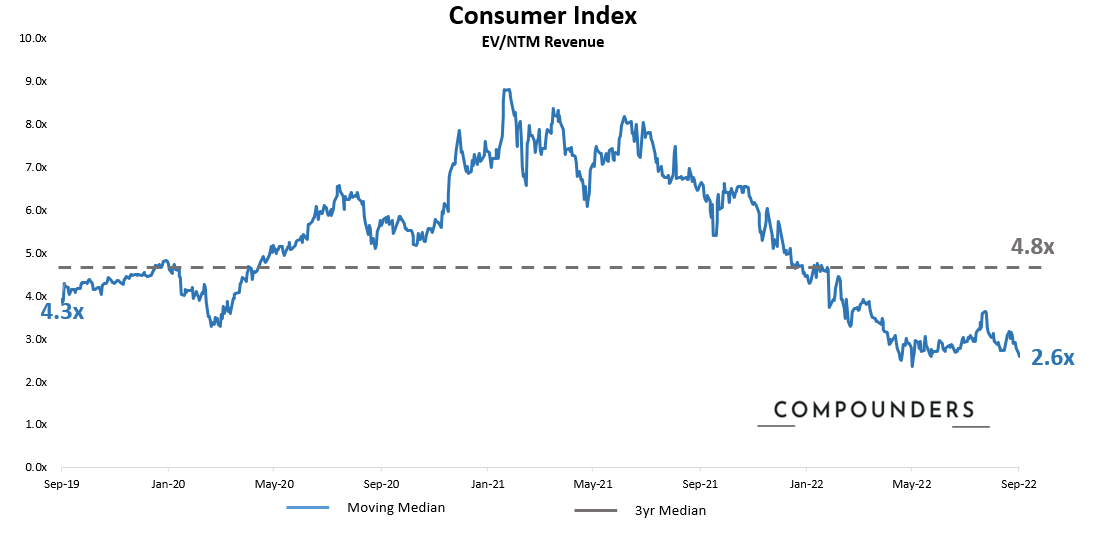

Also a near-term low at the Consumer index - dropping from last week’s 2.8x to 2.6x vs. all-time at 2.4x.

(Market data as of 9/23/2022, source: Bloomberg, CapIQ. See index composition at the bottom)

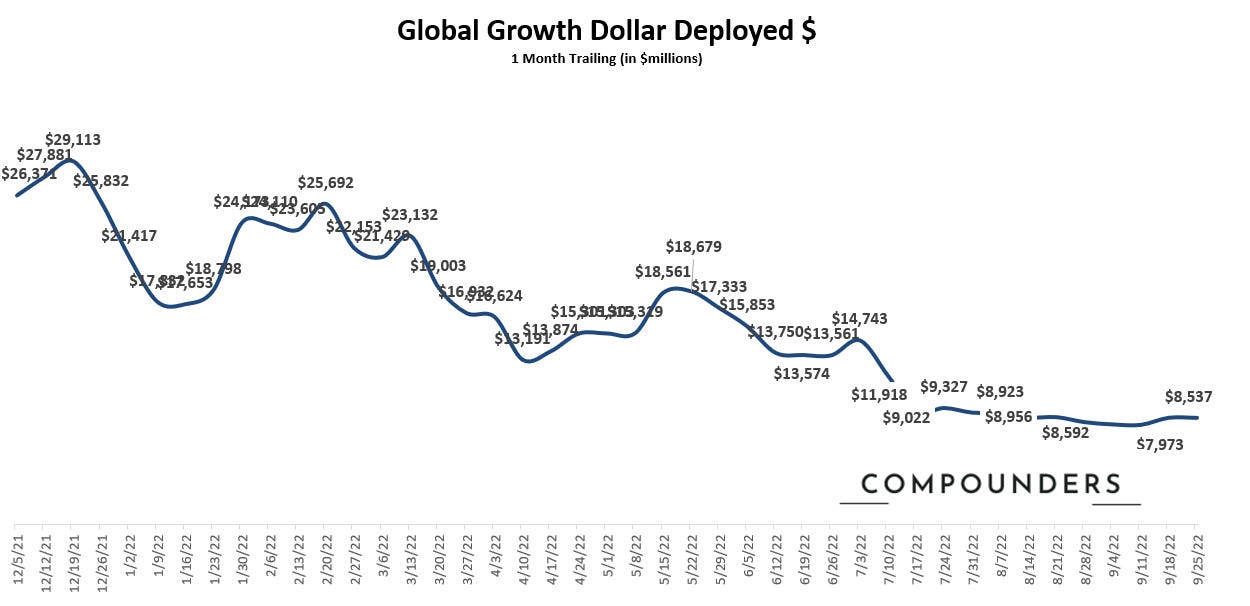

Chart of the Week in Private Market

(Deal data as of 09/25/2022, source: Pitchbook. Defined as - Series B+ global growth stage deals)

Some stability in the private market this week - Global Growth dollar deployed and deal announcements stayed at around $8B for the past trailing month this week. We continue to monitor this into late Sep / early Oct - to see if the floodgate of dry powder will eventually open for startups all around the world.

Sources: Software Index: over 200+ public companies / Fintech Index: V, MA, PYPL, SQ, BILL, ADYEN, SHOP, LSPD / Consumer Index: ABNB, BMBL, CHWY, CVNA, DASH, DHER, DKNG, DUOL, ETSY, FB, FTCH, GDRX, GOOGL, MTCH, NFLX, OPEN, PINS, POSH, PTON, ROKU, SFIX, SNAP, SPOT, UBER, W. Please feel free to ping us for further detailed breakdown