Compounders 2.20.22

To stay in touch, you can find us here: GZ's Twitter and Shan’s Twitter

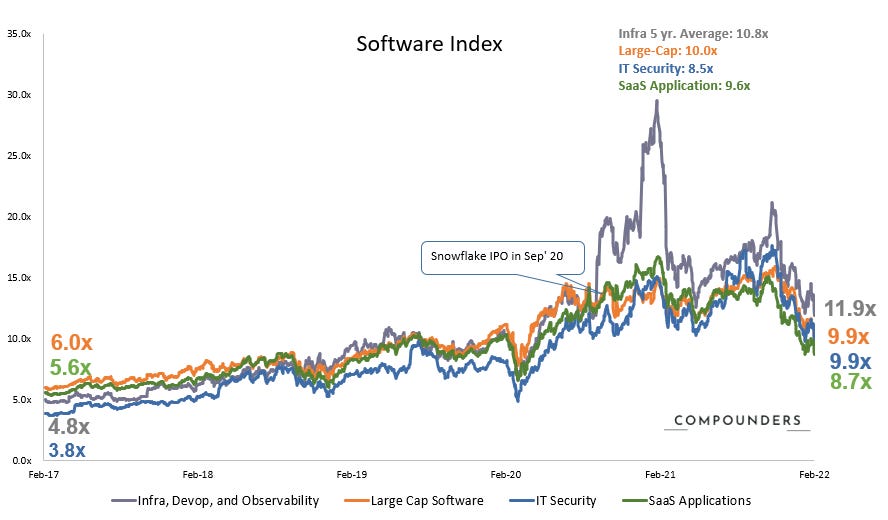

Chart of the Week in the Public Market

Software Index experienced a sector-wide correction this week. Infrastructure contracted the most from 13.2x to 11.9x. Large-cap names, investors’ favorite hiding place, retreated from 11.0x to 9.9x. IT security and SaaS followed the broader sell-off and came out at 9.9x and 8.7x, respectively.

Fintech Index EV/Fwd Rev further contracted this week from 16.3x to 14.3x, now drawing close to 2019 and below median 18.4x. Beyond just growth stocks, value stocks like Card Network and Merchant Acquirer/Processor also started to see pullback. FIS guided Q1 below street estimates and reported merchant vol +17% yoy.

Consumer Index EV/Fwd Rev saw a substantial drop this week from 4.6x to 3.8x, below 2019 and 3-year median. Big week for internet earnings - RBLX sold off to slowing users growth and commentary that it expected continued slower growth until 2H:22. ABNB delivered better than expected top-line and bottom line profiles - nights and experiences guides for Q1-22 will be 25% above ‘19 levels. Divergences are starting to form between sectors and companies for a post-COVID era. See more details below

(market data as of 2/18/2022, source: Bloomberg, CapIQ. See index composition at the bottom)

Public Market Commentary: Volatility continues, two storylines evolve

“Volatile” is an understatement to describe last week’s tech stocks performance. More than 20 tech stocks were down more than 20%. Some of the significant moving stocks include FSLY (-32%), ROKU (-22%), FUBO (-20%), SHOP (-22%),RBLX (-27%) and WIX (-26%). We observe two main storylines here:

1. Post-COVID Era: Pure COVID beneficiaries started to fade while travel and food services names held up well, forming a clear bifurcation. ROKU (-22%), FUBO (-20%), SHOP (-22%),RBLX (-27%) and WIX (-26%) suffered from slowing growth and weak guidance. TV and ScreenTime names took the heaviest hit. Interestingly, ABNB (+5%) and DASH (1%) came out of earnings intact. Companies like Salesforce emphasized selling “face to face” and hosted their corporate meeting recently in NYC. We think many tech companies will follow the trend and create stronger business travel demand. DASH stock shot up 30% AH following a solid print but fell back to pre-earnings due to concerns over rising competition post-COVID and missing EBITDA.

2. Recent IPO Class: Recent IPO software names continue to underperform, and the trend jumps out more noticeably following Confluent and Amplitude’s earnings. Looking at this week alone, a significant number of software market movers are recently IPO’ed companies - AMPL (-53%), HCP (-20%), CFLT (another -18% following prior week’s 25% sell-off), PLTR (-15%), GTLB (-16%). Here are some of our hypothesis around the current market environments:

Deal count spike != high quality assets. 109 companies went public in 2021, compared to 34 IPOs in 2019 and 46 IPOs in 2020. While we all love liquidity, unicorns aren’t created overnight. 77% of 2021 IPOs trade below IPO price. At the same time, SPAC redemption continues to climb to a horrendous 70-90% level. We have discussed this topic in depth in our previous issue (here).

The shift of the bull/bear market sentiment. Investors pay a premium for “story stocks” in a bull market - the ones with large TAM, less proven market (category definers), hypergrowth, and a massive cash burn. Under a bear market, however, investors go back to valuation drivers and seek durability in growth and sustainable cash flow.

Learned process of public reporting. Management teams are still learning how to interact with investors, provide proper guidance, and scale an organization effectively. It will take time to gain comfort as a management team to the public quarterly cadence. And time may not always be on their side with investors turning more conservative and rushing to large-cap safe haven.

Chart of the Week in Private Market

(Deal data as of 02/20/2022, source: Pitchbook. Defined as - Series B+ global growth stage deals)

Private Market Commentary:

Private market saw a gradual climb of global private deals announcement and growth dollars deployed. The latest 1 month trailing data would imply that the early Feb deployment velocity is slowly coming back. Some fundraising/business announcements we are watching this week are (note: valuation in post-money unless otherwise specified):

1. Super Bowl and the Dancing QR Code: Though not marketing majors, GZ and I both pay attention to Super Bowl each year as it functions as a strong indicator for consumer spending/consumer brand. This year - many called the event “Fintech Bowl” or “Crypto Bowl”. With a price tag of $7 million each (source), these 30-second ad slots are being bought by some of the fastest rising companies in the world. Coinbase topped the post-event download growth chart (+309%, source), winning buzz and the customer acquisition game. Fintech/crypto companies like eToro, FTX, and Greenlight also saw substantial boosts though this marketing event. How to grow organically and virally will forever be the billion dollar question in consumer internet companies. And this year, it seems like one of the possible tricks is to evoke the curious nature of human beings.

2. Crypto Payments : So much of the buzz generated around Crypto in the last two years has been around trading, HOLDing, and NFTs. These transactions and conversations have significantly pushed the ecosystem forward and catalyzed innovations. But it’s worth reminding ourselves that another important frontier of the industry centers around better payments. Cross-border payments, low-cost remittances, stable currencies were some of the first-use cases as well as visions of the ecosystem from day 1. These offerings and products may be slower to hit the market and generate hype - but they are striving to create real value to people and companies all around the world.

On the positive side - Crypto custodian Fireblocks announced this week the $100M acquisition of First Digital, an Isreali-based firm that allows companies to accept payments via Stablecoins. Merchants who use supported payment service providers can start to accept and make payments using crypto as soon as this spring. Broader vendors and merchants adoption could really accelerate the buildout of crypto as an underlying method of payment worldwide.

On the negative side - El Salvador became the first country to allow consumers to use cryptocurrency in all transactions in September, 2021. IMF recently issued a warning and urged El Salvador to strip Bitcoin of its status as legal currency, stating that otherwise it would be difficult to get a loan from the institution.

The road ahead for cryptocurrency to exhibit its fiscal and monetary value seems more zig-zagy than straight up to the right - but we believe compounders will be built where true values are being created.

3. The Future State of Consumer: Having now covered consumer companies across the public and private markets for years, I am still constantly amazed by the users as well as format growth of the consumer landscape. From 2011-2021, the smartphone sales have tripled to $1.54B. The US in total had 179M 3G subscribers in 2011 ( Internet Report) vs. today FB alone has 2.9B users today. The internet certainly grew exponentially larger and more diverse over the years and I am more excited than ever to see what’s next to come. Last section of the private market today, we want to recommend writings from an incredible fund - Forerunner. Their latest piece/announcement here.

Enjoy reading! Have a wonderful long weekend from the Compounders.

Sources: Software Index: over 200+ public companies / Fintech Index: V,MA,PYPL,SQ,BILL,ADYEN,SHOP,LSPD / Consumer Index: ABNB, BMBL, CHWY, CVNA, DASH, DHER, DKNG, DUOL, ETSY, FB, FTCH, GDRX, GOOGL, MTCH, NFLX, OPEN, PINS, POSH, PTON, ROKU, SFIX, SNAP, SPOT, UBER, W. Please feel free to ping us for further detailed breakdown